Derivative Pricing_2_Vasicek

*Catalog

1. Plotting Vasicek Trajectories

2. CKLS Method for Parameter Estimation (elaborated by GMM and Euler Approx)

3. Application

1. Plotting Vasicek Trajectories

(1) Basic outlooking:

vasicek <- function(alpha, beta, sigma, n = 100, r0 = 0.026) {

v <- rep(0, n)

v[1] <- r0

for (i in 2:n) {

v[i] <- v[i - 1] + alpha * (beta - v[i - 1]) + sigma * rnorm(1)

}

return(v)

}

set.seed(13)

r <- replicate(3, vasicek(0.02, 0.056, 0.0006))

# plot columns of matrix against columns of another matrix

matplot(r, type = 'l', ylab = '', xlab = 'Time', xaxt = 'no',

main = 'Simulation of Interest Rate Using Vasicek Trajectories')

lines(c(-1, 101), c(0.056, 0.056), col = 'grey', lwd = 2, lty = 1)

(2) Characteristics:

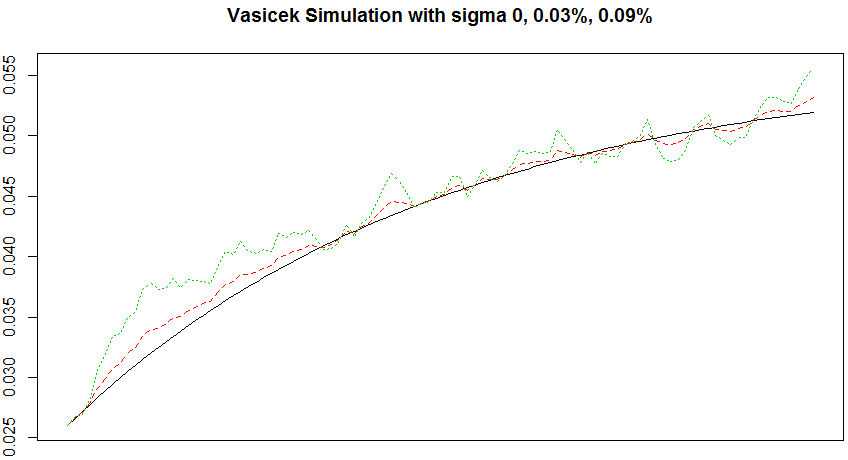

# change sigma (old sigma is 0.0006)

r <- sapply(c(0, 0.0003, 0.0009),

function(sigma){

set.seed(23); vasicek(0.02, 0.056, sigma)

})

matplot(r, type = 'l', ylab = '', xlab = 'Time', xaxt = 'no',

main = 'Vasicek Simulation with sigma 0, 0.03%, 0.09%')

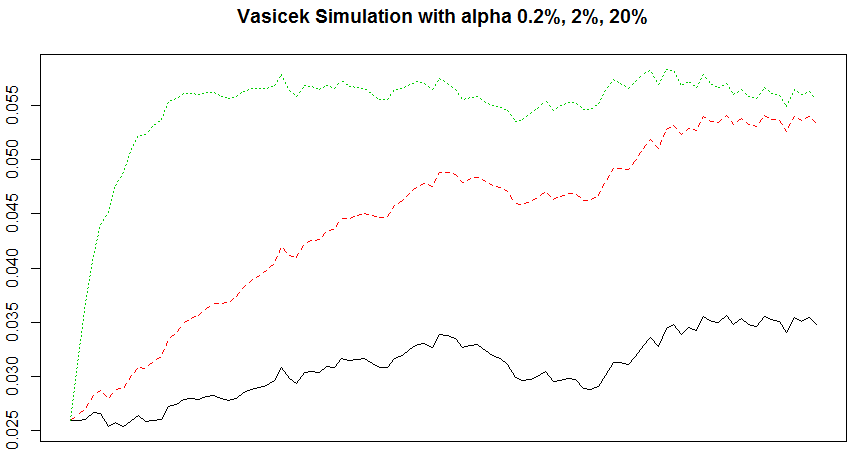

# change alpha (old alpha is 0.02)

r <- sapply(c(0.002, 0.02, 0.2),

function(alpha){

set.seed(33); vasicek(alpha, 0.056, 0.0006)

})

matplot(r, type = 'l', ylab = '', xlab = 'Time', xaxt = 'no',

main = 'Vasicek Simulation with alpha 0.2%, 2%, 20%')

(3) Comments:

This model is a continuous, affine and one-factor stochastic interest rate model.

It follows a mean-reverting process (expected value converges to beta when Time of alpha goes to infinity (alpha can be treated as speed of adjustment to the long-run beta). The higher alpha, the earlier reach long-term beta (which input by me as 0.056). As alpha goes infinity, variance converges to 0.

2. Parameter Estimation

(1) Generalized Method of Moments:

gamma = 0 in Vasicek model;

gamma = 0.5 in CIR model (which assumes that volatility term proportional to the square root of the interest rate level; and that interest rate has non-central

chi-squared distribution);

(2) Mechanism:

Denote a vector of parameters to be estimated, theta = (alpha, beta, sigma, gamma);

Set null hypothesis is : E[ Mt(theta) ] = 0;

Use a sample corresponding to E[ Mt(theta) ], which is denoted as mt(theta) = (1/n) * Σ Mt(theta), where t from 1 to n, and n is number of observations;

Introduce omega as a weight matrix, which is symmetric, positive and definite;

Thus, GMM minimize this quadratic term: mt(theta)Ω(theta)mt(theta);

3. Application

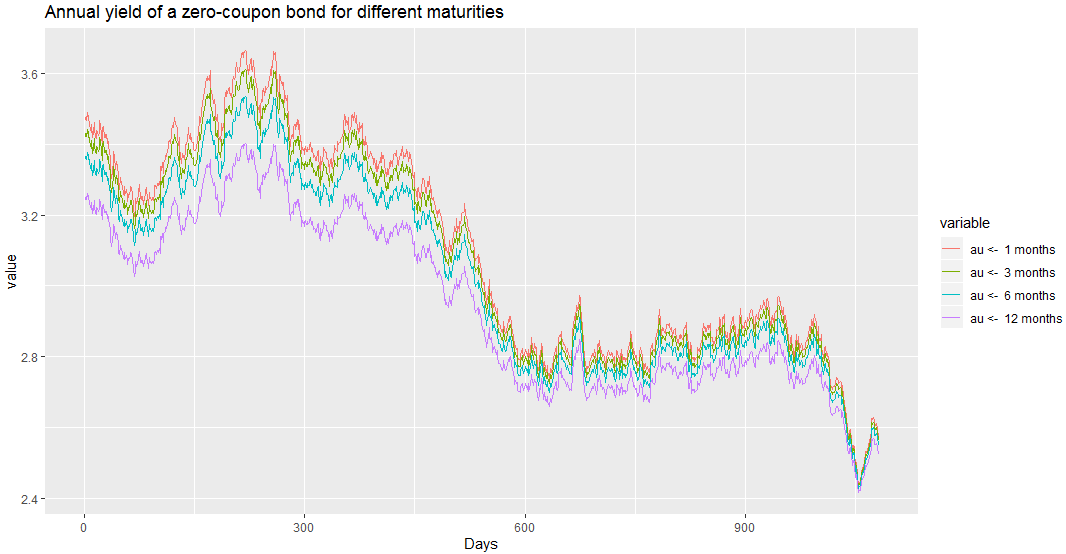

(1) Simulate bond prices with different maturities:

library(SMFI5)

a <- bond.vasicek(alpha = 0.5, beta = 2.55, sigma = 0.365, q1 = 0.3, q2 = 0,

r0 = 3.5, n = 1080, maturities = c(1/12, 3/12, 6/12, 1), days = 365)

plot(a)

Derivative Pricing_2_Vasicek的更多相关文章

- Derivative of the softmax loss function

Back-propagation in a nerual network with a Softmax classifier, which uses the Softmax function: \[\ ...

- Derivative of Softmax Loss Function

Derivative of Softmax Loss Function A softmax classifier: \[ p_j = \frac{\exp{o_j}}{\sum_{k}\exp{o_k ...

- XVII Open Cup named after E.V. Pankratiev Stage 14, Grand Prix of Tatarstan, Sunday, April 2, 2017 Problem A. Arithmetic Derivative

题目:Problem A. Arithmetic DerivativeInput file: standard inputOutput file: standard inputTime limit: ...

- The Softmax function and its derivative

https://eli.thegreenplace.net/2016/the-softmax-function-and-its-derivative/ Eli Bendersky's website ...

- matlab 提示 Continuous sample time is not supported by discrete derivative 错误的解决办法

Simulink仿真的时候,出行错误提示:Continuous sample time is not supported by discrete derivative 中文意思是:连续采样时间不支持离 ...

- [PE484]Arithmetic Derivative

题意:对整数定义求导因子$'$:$p'=1,(ab)'=a'b+ab'$,求$\sum\limits_{i=2}^n(i,i')$ 这个求导定义得比较妙:$(p^e)'=ep^{e-1}$ 推一下就可 ...

- 【找规律】【DFS】XVII Open Cup named after E.V. Pankratiev Stage 14, Grand Prix of Tatarstan, Sunday, April 2, 2017 Problem A. Arithmetic Derivative

假设一个数有n个质因子a1,a2,..,an,那么n'=Σ(a1*a2*...*an)/ai. 打个表出来,发现一个数x,如果x'=Kx,那么x一定由K个“基础因子”组成. 这些基础因子是2^2,3^ ...

- 共变导数(Covariant Derivative)

原文链接 导数是指某一点的导数表示了某点上指定函数的变化率. 比如,要确定某物体的速度在某时刻的加速度,就取时间轴上下一时刻的一个微小增量,然后考察速度的增量和时间增量的比值.如果这个比值比较大,说明 ...

- 求导四则运算以及三角函数求导 Derivative formulas

对特定函数的求导. 1:sin(x) 对其进行求斜率.带入公式得:[ sin(x+Δx)- sin(x)]/Δx = [ sinx*cosΔx + cosx*sinΔx -sin x ]/ Δx = ...

随机推荐

- P1157 组合的输出

P1157 组合的输出 #include <bits/stdc++.h> using namespace std; int n,r; int a[25]; vector<int> ...

- Node.js介绍、优势、用途

一.Node.js介绍Node.js是一个javascript运行环境.它让javascript可以开发后端程序,实现几乎其他后端语言实现的所有功能,可以与PHP.Java.Python..NET.R ...

- java实现文字转语音功能(仅Windows)

一.pom.xml引入jar包依赖 <!-- https://mvnrepository.com/artifact/com.jacob/jacob 文字转语音 --> <depend ...

- if条件语句!

1.if 单分支语句 if [ 条件语句 ] then 条件操作fi 例子: [root@localhost ~]# if [ 1 -eq 0 ] //如果1等 ...

- 01-JAVA语言基础(动手动脑)

一.一个JAVA类文件中只能有一个public类吗? 01-JAVA语言基础.ppt第22页“一个Java源文件中可以写多个类,但其中只能有一个类是“公有(public)”的,并且Java要求源文件名 ...

- bootstrap中col-xs-*和col-sm-* 和col-md-*是怎么样对应的

在做布局时,有时窗体大小变化会出现非想要的效果. 栅格系统中的列是通过指定1到12的值来表示其跨越的范围 所以不会有col-**-15 最大也就是12<div class="col-s ...

- NET站点升级后,新特新无法编译通过

NET3.5 webconfig中有自动配置如下代码,用于指示编译器. <system.codedom> <compilers> <compiler language=& ...

- uniGUI之通过URL控制参数(25)

通过URL代入参数,在代码中读取,如: http://localhost:8077/?ServerPort=212&&ServerIP=192.168.31.12 procedure ...

- [追热点]学习Rust之选择IDE

学习语言非常需要实际上手写代码,自然绕不开IDE工具,所以第一时间当然是选择IDE. Rust官网推荐 先去看看Rust官网推荐了什么IDE:工具 - Rust 程序设计语言 无论您喜欢用命令行还是可 ...

- Win10 在 CUDA 10.1 下跑 TensorFlow 2.x

深度学习最热的两个框架是 pytorch 和 tensorflow,pytorch 最新版本是 1.3,tensorflow 最新版本为 2.0,在 win10 下 pytorch 1.3 要求的 c ...