[Python] Statistical analysis of time series

Global Statistics:

Common seen methods as such

1. Mean

2. Median

3. Standard deviation: the larger the number means it various a lot.

4. Sum.

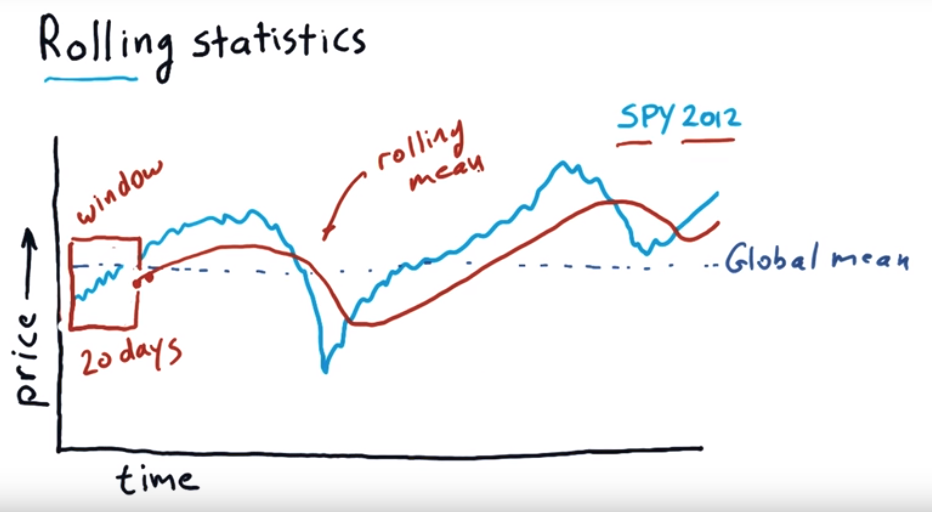

Rolling Statistics:

It use a time window, moving forward each day to calculate the mean value of those window periods.

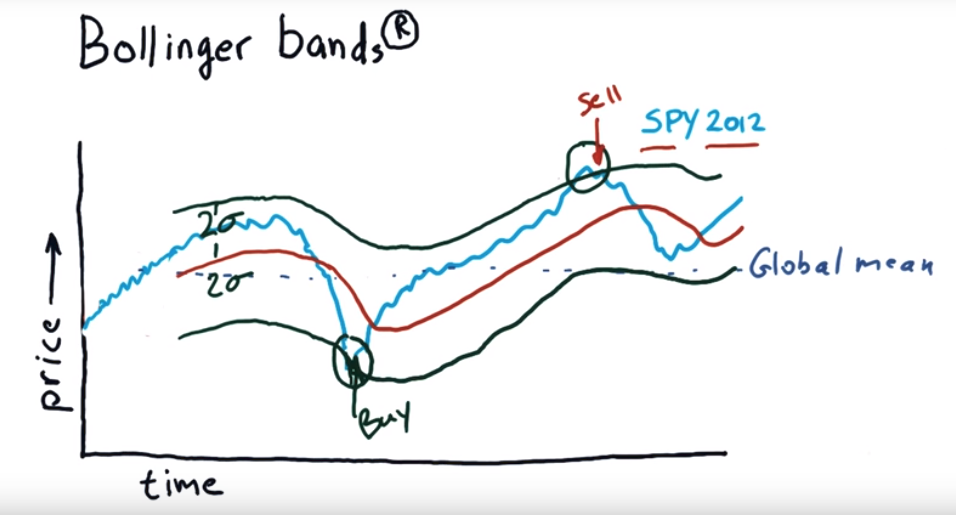

To find which day is good to buy which day is good for sell, we can use Bollinger bands.

Bollinger bands:

import os

import pandas as pd

import matplotlib.pyplot as plt def test_run():

start_date='2017-01-01'

end_data='2017-12-15'

dates=pd.date_range(start_date, end_data) # Create an empty data frame

df=pd.DataFrame(index=dates) symbols=['SPY', 'AAPL', 'IBM', 'GOOG', 'GLD']

for symbol in symbols:

temp=getAdjCloseForSymbol(symbol)

df=df.join(temp, how='inner') return df if __name__ == '__main__':

df=test_run()

# data=data.ix['2017-12-01':'2017-12-15', ['IBM', 'GOOG']]

# df=normalize_data(df)

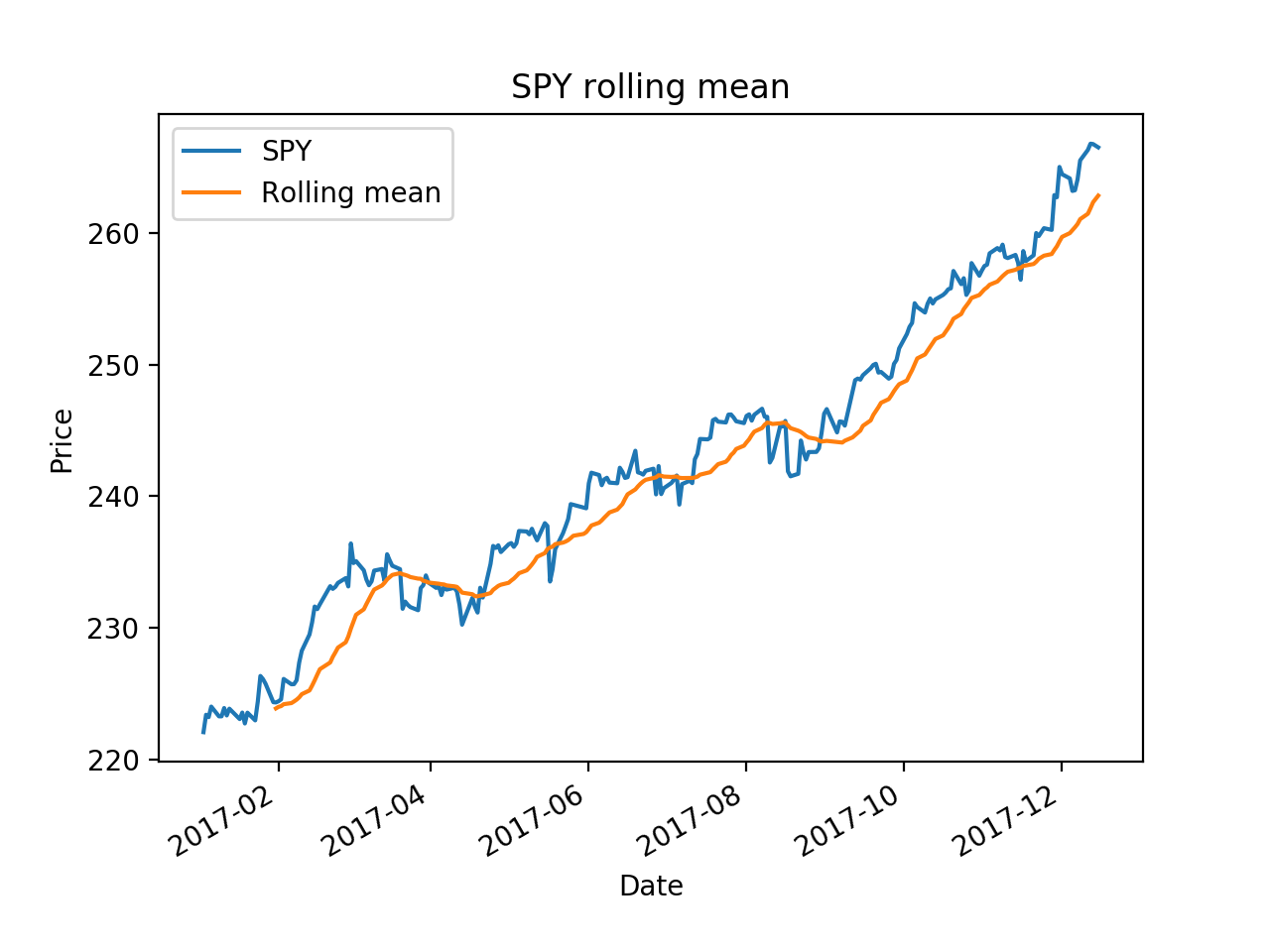

ax = df['SPY'].plot(title="SPY rolling mean", label='SPY')

rm = df['SPY'].rolling(20).mean()

rm.plot(label='Rolling mean', ax=ax)

ax.set_xlabel('Date')

ax.set_ylabel('Price')

ax.legend(loc="upper left")

plt.show()

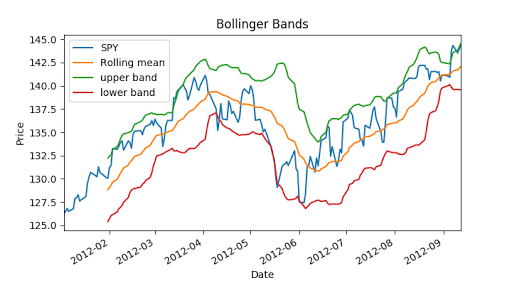

Now we can calculate Bollinger bands, it is 2 times std value.

"""Bollinger Bands.""" import os

import pandas as pd

import matplotlib.pyplot as plt def symbol_to_path(symbol, base_dir="data"):

"""Return CSV file path given ticker symbol."""

return os.path.join(base_dir, "{}.csv".format(str(symbol))) def get_data(symbols, dates):

"""Read stock data (adjusted close) for given symbols from CSV files."""

df = pd.DataFrame(index=dates)

if 'SPY' not in symbols: # add SPY for reference, if absent

symbols.insert(0, 'SPY') for symbol in symbols:

df_temp = pd.read_csv(symbol_to_path(symbol), index_col='Date',

parse_dates=True, usecols=['Date', 'Adj Close'], na_values=['nan'])

df_temp = df_temp.rename(columns={'Adj Close': symbol})

df = df.join(df_temp)

if symbol == 'SPY': # drop dates SPY did not trade

df = df.dropna(subset=["SPY"]) return df def plot_data(df, title="Stock prices"):

"""Plot stock prices with a custom title and meaningful axis labels."""

ax = df.plot(title=title, fontsize=12)

ax.set_xlabel("Date")

ax.set_ylabel("Price")

plt.show() def get_rolling_mean(values, window):

"""Return rolling mean of given values, using specified window size."""

return values.rolling(window=window).mean() def get_rolling_std(values, window):

"""Return rolling standard deviation of given values, using specified window size."""

# TODO: Compute and return rolling standard deviation

return values.rolling(window=window).std() def get_bollinger_bands(rm, rstd):

"""Return upper and lower Bollinger Bands."""

# TODO: Compute upper_band and lower_band

upper_band = rstd * 2 + rm

lower_band = rm - rstd * 2

return upper_band, lower_band def test_run():

# Read data

dates = pd.date_range('2012-01-01', '2012-12-31')

symbols = ['SPY']

df = get_data(symbols, dates) # Compute Bollinger Bands

# 1. Compute rolling mean

rm_SPY = get_rolling_mean(df['SPY'], window=20) # 2. Compute rolling standard deviation

rstd_SPY = get_rolling_std(df['SPY'], window=20) # 3. Compute upper and lower bands

upper_band, lower_band = get_bollinger_bands(rm_SPY, rstd_SPY) # Plot raw SPY values, rolling mean and Bollinger Bands

ax = df['SPY'].plot(title="Bollinger Bands", label='SPY')

rm_SPY.plot(label='Rolling mean', ax=ax)

upper_band.plot(label='upper band', ax=ax)

lower_band.plot(label='lower band', ax=ax) # Add axis labels and legend

ax.set_xlabel("Date")

ax.set_ylabel("Price")

ax.legend(loc='upper left')

plt.show() if __name__ == "__main__":

test_run()

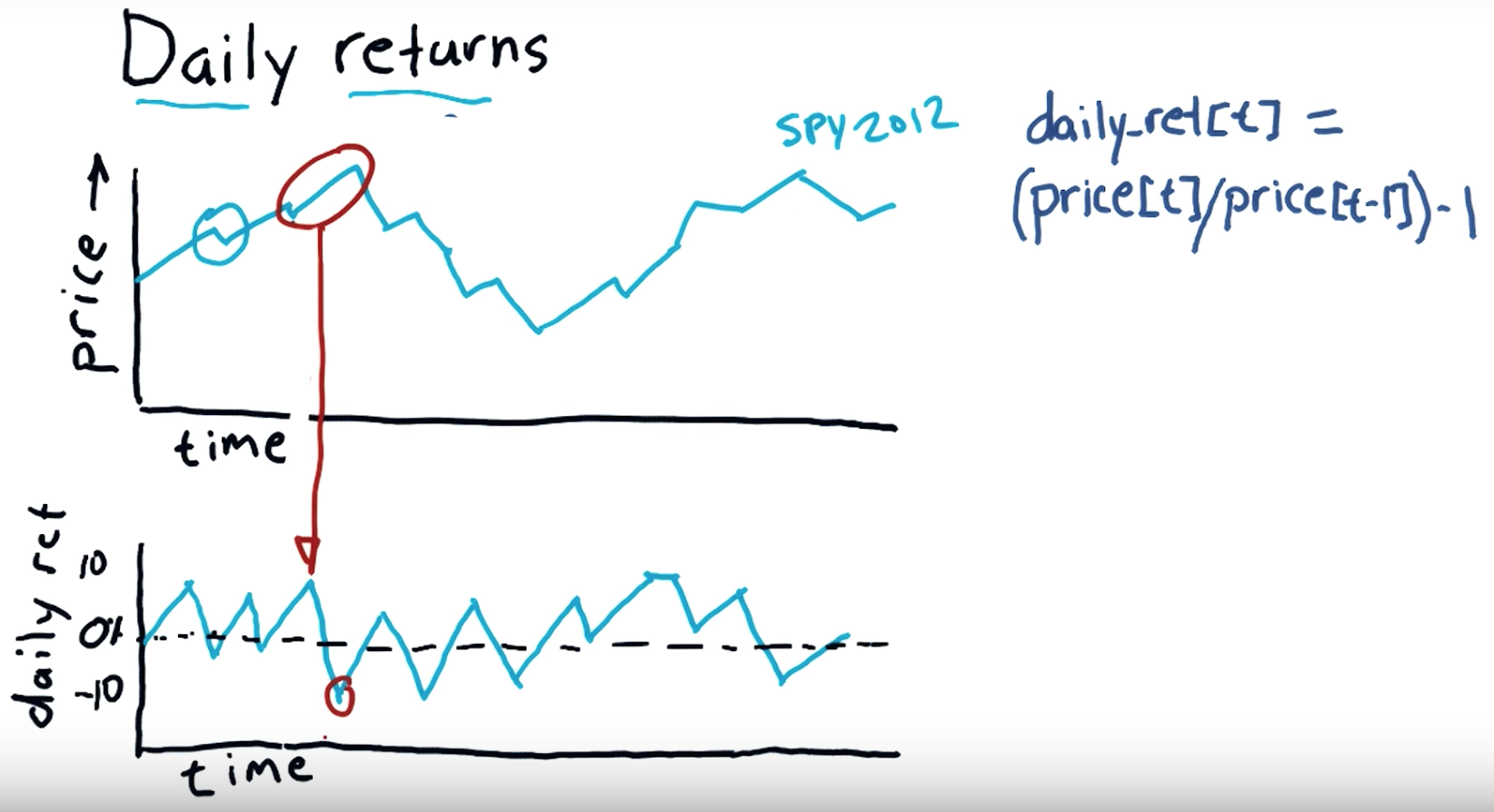

Daily return:

Subtract the previous day's closing price from the most recent day's closing price. In this example, subtract $35.50 from $36.75 to get $1.25. Divide your Step 4 result by the previous day's closing price to calculate the daily return. Multiply this result by 100 to convert it to a percentage.

"""Compute daily returns.""" import os

import pandas as pd

import matplotlib.pyplot as plt def symbol_to_path(symbol, base_dir="data"):

"""Return CSV file path given ticker symbol."""

return os.path.join(base_dir, "{}.csv".format(str(symbol))) def get_data(symbols, dates):

"""Read stock data (adjusted close) for given symbols from CSV files."""

df = pd.DataFrame(index=dates)

if 'SPY' not in symbols: # add SPY for reference, if absent

symbols.insert(0, 'SPY') for symbol in symbols:

df_temp = pd.read_csv(symbol_to_path(symbol), index_col='Date',

parse_dates=True, usecols=['Date', 'Adj Close'], na_values=['nan'])

df_temp = df_temp.rename(columns={'Adj Close': symbol})

df = df.join(df_temp)

if symbol == 'SPY': # drop dates SPY did not trade

df = df.dropna(subset=["SPY"]) return df def plot_data(df, title="Stock prices", xlabel="Date", ylabel="Price"):

"""Plot stock prices with a custom title and meaningful axis labels."""

ax = df.plot(title=title, fontsize=12)

ax.set_xlabel(xlabel)

ax.set_ylabel(ylabel)

plt.show() def compute_daily_returns(df):

"""Compute and return the daily return values."""

# TODO: Your code here

# Note: Returned DataFrame must have the same number of rows

return df / df.shift(-1) -1 def test_run():

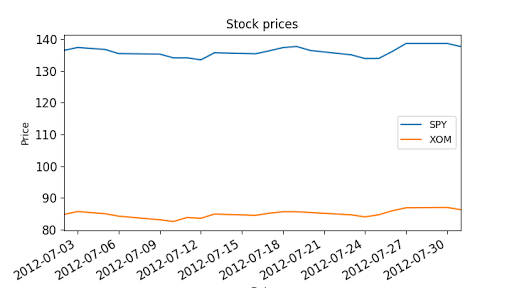

# Read data

dates = pd.date_range('2012-07-01', '2012-07-31') # one month only

symbols = ['SPY','XOM']

df = get_data(symbols, dates)

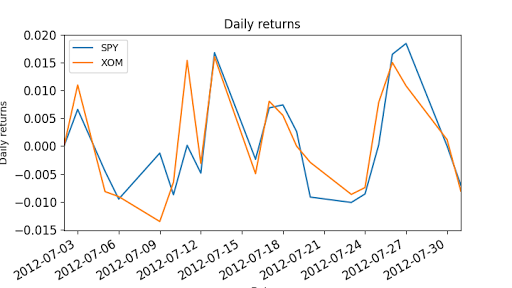

plot_data(df) # Compute daily returns

daily_returns = compute_daily_returns(df)

plot_data(daily_returns, title="Daily returns", ylabel="Daily returns") if __name__ == "__main__":

test_run()

Cumulative return:

an investment relative to the principal amount invested over a specified amount of time. ... To calculate cumulative return, subtract the original price of the investment from the current price and divide that difference by the original price.

[Python] Statistical analysis of time series的更多相关文章

- How-to: Do Statistical Analysis with Impala and R

sklearn实战-乳腺癌细胞数据挖掘(博客主亲自录制视频教程) https://study.163.com/course/introduction.htm?courseId=1005269003&a ...

- python data analysis | python数据预处理(基于scikit-learn模块)

原文:http://www.jianshu.com/p/94516a58314d Dataset transformations| 数据转换 Combining estimators|组合学习器 Fe ...

- python学习笔记—DataFrame和Series的排序

更多大数据分析.建模等内容请关注公众号<bigdatamodeling> ################################### 排序 ################## ...

- Should You Build Your Own Backtester?

By Michael Halls-Moore on August 2nd, 2016 This post relates to a talk I gave in April at QuantCon 2 ...

- Python数据分析工具:Pandas之Series

Python数据分析工具:Pandas之Series Pandas概述Pandas是Python的一个数据分析包,该工具为解决数据分析任务而创建.Pandas纳入大量库和标准数据模型,提供高效的操作数 ...

- 用 Python 通过马尔可夫随机场(MRF)与 Ising Model 进行二值图降噪

前言 这个降噪的模型来自 Christopher M. Bishop 的 Pattern Recognition And Machine Learning (就是神书 PRML……),问题是如何对一个 ...

- 大数据分析与机器学习领域Python兵器谱

http://www.thebigdata.cn/JieJueFangAn/13317.html 曾经因为NLTK的缘故开始学习Python,之后渐渐成为我工作中的第一辅助脚本语言,虽然开发语言是C/ ...

- Machine and Deep Learning with Python

Machine and Deep Learning with Python Education Tutorials and courses Supervised learning superstiti ...

- Python 网页爬虫 & 文本处理 & 科学计算 & 机器学习 & 数据挖掘兵器谱(转)

原文:http://www.52nlp.cn/python-网页爬虫-文本处理-科学计算-机器学习-数据挖掘 曾经因为NLTK的缘故开始学习Python,之后渐渐成为我工作中的第一辅助脚本语言,虽然开 ...

随机推荐

- CDR X6设计师的福利,3折特惠!

最新消息称,即日起CorelDRAW官方为回馈新老用户长期以来的支持,特别推出CorelDRAW X6降价活动.目前CorelDRAW X6售价仅为2399元,照这个价格,CDR 2017 会 ...

- html5学习之第一步:认识标签,了解布局

图1. Acme United的网页的规划 Header区的例子包含了页面标题和副标题,< header>标签被用来创建页面的Header区的内容.除了网页本身之外,< header ...

- pip 出错

pip 升级到10以上出错 ImportError: cannot import name 'main' 解决方法一: 降低pip的版本号 python -m pip install pip==9.0 ...

- 洛谷 P3914 染色计数

P3914 染色计数 题目描述 有一颗NN个节点的树,节点用1,2,\cdots,N1,2,⋯,N编号.你要给它染色,使得相邻节点的颜色不同.有MM种颜色,用1,2,\cdots,M1,2,⋯,M编号 ...

- Python 入门学习 -----变量及基础类型(元组,列表,字典,集合)

Python的变量和数据类型 1 .python的变量是不须要事先定义数据类型的.能够动态的改变 2. Python其中一切皆对象,变量也是一个对象,有自己的属性和方法 我们能够通过 来查看变量的类型 ...

- 与Greenplum度过的三个星期

5月4日-5月24日.断断续续折腾了三个星期的Greenplum,总算告一段落了:扩容,发现扩不成容.仅仅好升级.升级,发现一堆错误,仅仅好暂停修复数据库:修好了,继续升级.升完级,发现错误.修啊修啊 ...

- ZOJ2326Tangled in Cables(最小生成树)

Tangled in Cables Time Limit: 2 Seconds Memory Limit: 65536 KB You are the owner of SmallCableC ...

- 智课雅思词汇---十一、spect是什么意思

智课雅思词汇---十一.spect是什么意思 一.总结 一句话总结:词根:spect, speci, spec(spic, spi, spy) = to look, to see 看 1.port是什 ...

- 监控rman备份

1.服务会话关联通道设置 set COMMAND ID 命令 2.查询V$PROCESS和V$SESSION 决定会话对应的RMAN的通道 3.查询V$session_LONGGOPS监控备份集和复制 ...

- PostgreSQL源代码中插件的使用

如果编译数据库时使用了gmake world和gmake install-world, 所有的插件都会被安装, 那么就不需要再次安装了. 插件目录 contrib 进入要安装的插件目录, 例如 cd ...