分位数回归及其Python源码

分位数回归及其Python源码

天朗气清,惠风和畅。赋闲在家,正宜读书。前人文章,不得其解。代码开源,无人注释。你们不来,我行我上。废话少说,直入主题。o( ̄︶ ̄)o

我们要探测自变量 与因变量

的关系,最简单的方法是线性回归,即假设:

我们通过最小二乘方法 (OLS: ordinary least squares), 的可靠性问题,我们同时对残差

做了假设,即:

为均值为0,方差恒定的独立随机变量。

即为给定自变量

下,因变量

的条件均值。

假如残差 不满足我们的假设,或者更重要地,我们不仅仅想要知道

的在给定

下的条件均值,而且想知道是条件中位数(更一般地,条件分位数),那么OLS下的线性回归就不能满足我们的需求。分位数回归(Quantile Regression)[2]解决了这些问题,下面我先给出一个分位数回归的实际应用例子,再简述其原理,最后再分析其在Python实现的源代码。

1. 一个例子:收入与食品消费

这个例子出自statasmodels:Quantile Regression.[3] 我们想探索家庭收入与食品消费的关系,数据出自working class Belgian households in 1857 (the Engel data).我们用Python包statsmodels实现分位数回归。

1.1 预处理

%matplotlib inline

import numpy as np

import pandas as pd

import statsmodels.api as sm

import statsmodels.formula.api as smf

import matplotlib.pyplot as plt

data = sm.datasets.engel.load_pandas().data

data.head()

income foodexp

0 420.157651 255.839425

1 541.411707 310.958667

2 901.157457 485.680014

3 639.080229 402.997356

4 750.875606 495.560775

1.2 中位数回归 (分位数回归的特例,q=0.5)

mod = smf.quantreg('foodexp ~ income', data)

res = mod.fit(q=.5)

print(res.summary())

QuantReg Regression Results

==============================================================================

Dep. Variable: foodexp Pseudo R-squared: 0.6206

Model: QuantReg Bandwidth: 64.51

Method: Least Squares Sparsity: 209.3

Date: Mon, 21 Oct 2019 No. Observations: 235

Time: 17:46:59 Df Residuals: 233

Df Model: 1

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 81.4823 14.634 5.568 0.000 52.649 110.315

income 0.5602 0.013 42.516 0.000 0.534 0.586

==============================================================================

The condition number is large, 2.38e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

由结果可以知道 ,如何得到回归系数的估计?结果中的std err, t, Pseudo R-squared等是什么?我会在稍后解释。

1.3 数据可视化

我们先拟合10个分位数回归,分位数q分别在0.05到0.95之间。

quantiles = np.arange(.05, .96, .1)

def fit_model(q):

res = mod.fit(q=q)

return [q, res.params['Intercept'], res.params['income']] + \

res.conf_int().loc['income'].tolist()

models = [fit_model(x) for x in quantiles]

models = pd.DataFrame(models, columns=['q', 'a', 'b', 'lb', 'ub'])

ols = smf.ols('foodexp ~ income', data).fit()

ols_ci = ols.conf_int().loc['income'].tolist()

ols = dict(a = ols.params['Intercept'],

b = ols.params['income'],

lb = ols_ci[0],

ub = ols_ci[1])

print(models)

print(ols)

q a b lb ub

0 0.05 124.880096 0.343361 0.268632 0.418090

1 0.15 111.693660 0.423708 0.382780 0.464636

2 0.25 95.483539 0.474103 0.439900 0.508306

3 0.35 105.841294 0.488901 0.457759 0.520043

4 0.45 81.083647 0.552428 0.525021 0.579835

5 0.55 89.661370 0.565601 0.540955 0.590247

6 0.65 74.033435 0.604576 0.582169 0.626982

7 0.75 62.396584 0.644014 0.622411 0.665617

8 0.85 52.272216 0.677603 0.657383 0.697823

9 0.95 64.103964 0.709069 0.687831 0.730306

{'a': 147.47538852370562, 'b': 0.48517842367692354, 'lb': 0.4568738130184233,

这里拟合了10个回归,其中q是对应的分位数,a是斜率,b是回归系数。lb和ub分别是b的95%置信区间的下界与上界。

现在来画出这10条回归线:

x = np.arange(data.income.min(), data.income.max(), 50)

get_y = lambda a, b: a + b * x

fig, ax = plt.subplots(figsize=(8, 6))

for i in range(models.shape[0]):

y = get_y(models.a[i], models.b[i])

ax.plot(x, y, linestyle='dotted', color='grey')

y = get_y(ols['a'], ols['b'])

ax.plot(x, y, color='red', label='OLS')

ax.scatter(data.income, data.foodexp, alpha=.2)

ax.set_xlim((240, 3000))

ax.set_ylim((240, 2000))

legend = ax.legend()

ax.set_xlabel('Income', fontsize=16)

ax.set_ylabel('Food expenditure', fontsize=16);

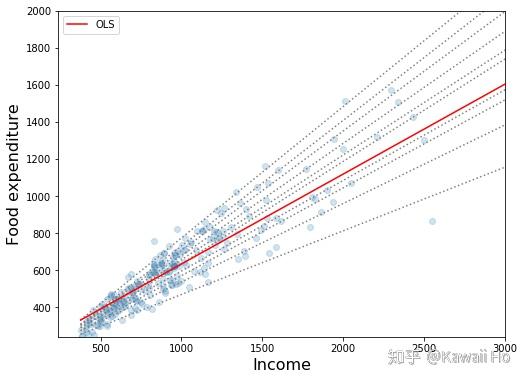

上图中虚线是分位数回归线,红线是线性最小二乘(OLS)的回归线。通过观察,我们可以发现3个现象:

- 随着收入提高,食品消费也在提高。

- 随着收入提高,家庭间食品消费的差别拉大。穷人别无选择,富人能选择生活方式,有喜欢吃贵的,也有喜欢吃便宜的。然而我们无法通过OLS发现这个现象,因为它只给了我们一个均值。

- 对与穷人来说,OLS预测值过高。这是因为少数的富人拉高了整体的均值,可见OLS对异常点敏感,不是一个稳健的模型。

2.分位数回归的原理

这部分是数理统计的内容,只关心如何实现的朋友可以略过。我们要解决以下这几个问题:

- 什么是分位数?

- 如何求分位数?

- 什么是分位数回归?

- 分位数回归的回归系数如何求得?

- 回归系数的检验如何进行?

- 如何评估回归拟合优度?

2.1 分位数的定义]

是随机变量,

的累积密度函数是

.

的

分位数为:

,

假设有100个人,95%的人身高少于1.9m, 1.9m就是身高的95%分位数。

2.2 分位数的求法

通过选择不同的 值,使

最小,对应的

值即为

的

分位数的估计

.

2.3 分位数回归

对于OLS, 我们有:

为

最小化所对应的

,类比地,对于

分位数回归,我们有:

为最小化:

即最小化

所对应的

2.4 系数估计

由于 不能直接对

求导,我们只能用迭代的方法来逼近

最小时对应的

值。statsmodels采用了Iteratively reweighted least squares (IRLS)的方法。

假设我们要求 最小化形如下的

范数:

则第t+1步迭代的 值为:

是对角矩阵且初始值为

第t次迭代

以中位数回归为例子(q=0.5),我们求:

即

即最小化形如上的 范数,

为避免分母为0,我们取 ,

是一个很小的数,例如0.0001.

2.5 回归系数的检验

我们通过2.4,多次迭代得出 的估计值,为了得到假设检验的t统计量,我们只需得到

的方差的估计。

分位数回归

的协方差矩阵的渐近估计为:

其中 是对角矩阵,

当 ,

, 当

,

的估计为

其中

为核函数(Kernel),可取Epa,Gaussian等.

为根据Stata 12所选的窗宽(bandwidth)[5]

回归结果中的std err即由 获得,t统计量等于

。

2.6 拟合优度

对于OLS,我们用 来衡量拟合优度。对于

分位数回归,我们类比得到:

,其中

为所有

观察值的

分位数。

即为回归结果中的Pseudo R-squared。

3.Python源码分析

实现分位数回归的完整源码在 ,里面主要含有两个类QuantReg 和 QuantRegResults. 其中QuantReg是核心,包含了回归系数估计,协方差计算等过程。QuantRegResults计算拟合优度并组织回归结果。

3.1 QuantReg类

#QuantReg是包中RegressionModel的一个子类

class QuantReg(RegressionModel):

#计算回归系数及其协方差矩阵。q是分位数,vcov是协方差矩阵,默认robust即2.5的方法。核函数kernel默认

#epa,窗宽bandwidth默认hsheather.IRLS最大迭代次数默认1000,差值默认小于1e-6时停止迭代

def fit(self, q=.5, vcov='robust', kernel='epa', bandwidth='hsheather',

max_iter=1000, p_tol=1e-6, **kwargs):

"""

Solve by Iterative Weighted Least Squares

Parameters

----------

q : float

Quantile must be between 0 and 1

vcov : str, method used to calculate the variance-covariance matrix

of the parameters. Default is ``robust``:

- robust : heteroskedasticity robust standard errors (as suggested

in Greene 6th edition)

- iid : iid errors (as in Stata 12)

kernel : str, kernel to use in the kernel density estimation for the

asymptotic covariance matrix:

- epa: Epanechnikov

- cos: Cosine

- gau: Gaussian

- par: Parzene

bandwidth : str, Bandwidth selection method in kernel density

estimation for asymptotic covariance estimate (full

references in QuantReg docstring):

- hsheather: Hall-Sheather (1988)

- bofinger: Bofinger (1975)

- chamberlain: Chamberlain (1994)

"""

if q < 0 or q > 1:

raise Exception('p must be between 0 and 1')

kern_names = ['biw', 'cos', 'epa', 'gau', 'par']

if kernel not in kern_names:

raise Exception("kernel must be one of " + ', '.join(kern_names))

else:

kernel = kernels[kernel]

if bandwidth == 'hsheather':

bandwidth = hall_sheather

elif bandwidth == 'bofinger':

bandwidth = bofinger

elif bandwidth == 'chamberlain':

bandwidth = chamberlain

else:

raise Exception("bandwidth must be in 'hsheather', 'bofinger', 'chamberlain'")

#endog样本因变量,exog样本自变量

endog = self.endog

exog = self.exog

nobs = self.nobs

exog_rank = np.linalg.matrix_rank(self.exog)

self.rank = exog_rank

self.df_model = float(self.rank - self.k_constant)

self.df_resid = self.nobs - self.rank

#IRLS初始化

n_iter = 0

xstar = exog

beta = np.ones(exog_rank)

# TODO: better start, initial beta is used only for convergence check

# Note the following does not work yet,

# the iteration loop always starts with OLS as initial beta

# if start_params is not None:

# if len(start_params) != rank:

# raise ValueError('start_params has wrong length')

# beta = start_params

# else:

# # start with OLS

# beta = np.dot(np.linalg.pinv(exog), endog)

diff = 10

cycle = False

history = dict(params = [], mse=[])

#IRLS迭代

while n_iter < max_iter and diff > p_tol and not cycle:

n_iter += 1

beta0 = beta

xtx = np.dot(xstar.T, exog)

xty = np.dot(xstar.T, endog)

beta = np.dot(pinv(xtx), xty)

resid = endog - np.dot(exog, beta)

mask = np.abs(resid) < .000001

resid[mask] = ((resid[mask] >= 0) * 2 - 1) * .000001

resid = np.where(resid < 0, q * resid, (1-q) * resid)

resid = np.abs(resid)

#1/resid[:, np.newaxis]为更新权重W

xstar = exog / resid[:, np.newaxis]

diff = np.max(np.abs(beta - beta0))

history['params'].append(beta)

history['mse'].append(np.mean(resid*resid))

#检查是否收敛,若收敛则提前停止迭代

if (n_iter >= 300) and (n_iter % 100 == 0):

# check for convergence circle, should not happen

for ii in range(2, 10):

if np.all(beta == history['params'][-ii]):

cycle = True

warnings.warn("Convergence cycle detected", ConvergenceWarning)

break

if n_iter == max_iter:

warnings.warn("Maximum number of iterations (" + str(max_iter) +

") reached.", IterationLimitWarning)

#计算协方差矩阵

e = endog - np.dot(exog, beta)

# Greene (2008, p.407) writes that Stata 6 uses this bandwidth:

# h = 0.9 * np.std(e) / (nobs**0.2)

# Instead, we calculate bandwidth as in Stata 12

iqre = stats.scoreatpercentile(e, 75) - stats.scoreatpercentile(e, 25)

h = bandwidth(nobs, q)

h = min(np.std(endog),

iqre / 1.34) * (norm.ppf(q + h) - norm.ppf(q - h))

fhat0 = 1. / (nobs * h) * np.sum(kernel(e / h))

if vcov == 'robust':

d = np.where(e > 0, (q/fhat0)**2, ((1-q)/fhat0)**2)

xtxi = pinv(np.dot(exog.T, exog))

xtdx = np.dot(exog.T * d[np.newaxis, :], exog)

vcov = chain_dot(xtxi, xtdx, xtxi)

elif vcov == 'iid':

vcov = (1. / fhat0)**2 * q * (1 - q) * pinv(np.dot(exog.T, exog))

else:

raise Exception("vcov must be 'robust' or 'iid'")

#用系数估计值和协方差矩阵创建一个QuantResults对象,并输出结果

lfit = QuantRegResults(self, beta, normalized_cov_params=vcov)

lfit.q = q

lfit.iterations = n_iter

lfit.sparsity = 1. / fhat0

lfit.bandwidth = h

lfit.history = history

return RegressionResultsWrapper(lfit)

#核函数表达式

def _parzen(u):

z = np.where(np.abs(u) <= .5, 4./3 - 8. * u**2 + 8. * np.abs(u)**3,

8. * (1 - np.abs(u))**3 / 3.)

z[np.abs(u) > 1] = 0

return z

kernels = {}

kernels['biw'] = lambda u: 15. / 16 * (1 - u**2)**2 * np.where(np.abs(u) <= 1, 1, 0)

kernels['cos'] = lambda u: np.where(np.abs(u) <= .5, 1 + np.cos(2 * np.pi * u), 0)

kernels['epa'] = lambda u: 3. / 4 * (1-u**2) * np.where(np.abs(u) <= 1, 1, 0)

kernels['gau'] = lambda u: norm.pdf(u)

kernels['par'] = _parzen

#kernels['bet'] = lambda u: np.where(np.abs(u) <= 1, .75 * (1 - u) * (1 + u), 0)

#kernels['log'] = lambda u: logistic.pdf(u) * (1 - logistic.pdf(u))

#kernels['tri'] = lambda u: np.where(np.abs(u) <= 1, 1 - np.abs(u), 0)

#kernels['trw'] = lambda u: 35. / 32 * (1 - u**2)**3 * np.where(np.abs(u) <= 1, 1, 0)

#kernels['uni'] = lambda u: 1. / 2 * np.where(np.abs(u) <= 1, 1, 0)

#窗宽计算

def hall_sheather(n, q, alpha=.05):

z = norm.ppf(q)

num = 1.5 * norm.pdf(z)**2.

den = 2. * z**2. + 1.

h = n**(-1. / 3) * norm.ppf(1. - alpha / 2.)**(2./3) * (num / den)**(1./3)

return h

def bofinger(n, q):

num = 9. / 2 * norm.pdf(2 * norm.ppf(q))**4

den = (2 * norm.ppf(q)**2 + 1)**2

h = n**(-1. / 5) * (num / den)**(1. / 5)

return h

def chamberlain(n, q, alpha=.05):

return norm.ppf(1 - alpha / 2) * np.sqrt(q*(1 - q) / n)

3.2 QuantRegResults类

这里我只给出计算拟合优度的代码。

class QuantRegResults(RegressionResults):

'''Results instance for the QuantReg model'''

@cache_readonly

def prsquared(self):

q = self.q

endog = self.model.endog

#e为残差

e = self.resid

e = np.where(e < 0, (1 - q) * e, q * e)

e = np.abs(e)

ered = endog - stats.scoreatpercentile(endog, q * 100)

ered = np.where(ered < 0, (1 - q) * ered, q * ered)

ered = np.abs(ered)

return 1 - np.sum(e) / np.sum(ered)

4.总结

上文我先给出了一个分位数回归的应用例子,进而叙述了分位数回归的原理,最后再分析了Python实现的源码。

分位数回归对比起OLS回归,虽然较为复杂,但它有三个主要优势:

- 能反映因变量分位数与自变量的关系,而不仅仅反映因变量均值与自变量的关系。

- 分位数回归对残差不作任何假设。

- 分位数回归受异常点的影响较小。

参考

- ^https://en.wikipedia.org/wiki/Ordinary_least_squares

- ^QUANTILE REGRESSION http://www.econ.uiuc.edu/~roger/research/rq/rq.pdf

- ^https://www.statsmodels.org/dev/examples/notebooks/generated/quantile_regression.html

- [1](https://www.zhihu.com/#ref_4_0)bchttps://en.wikipedia.org/wiki/Quantile_regression

- [2](https://www.zhihu.com/#ref_5_0)bchttps://www.statsmodels.org/devel/_modules/statsmodels/regression/quantile_regression.html

- ^https://en.wikipedia.org/wiki/Iteratively_reweighted_least_squares

- ^Green,W. H. (2008). Econometric Analysis. Sixth Edition. International Student Edition.

- ^https://www.ibm.com/support/knowledgecenter/en/SSLVMB_sub/statistics_mainhelp_ddita/spss/regression/idh_quantile.html

分位数回归及其Python源码的更多相关文章

- 读python源码--对象模型

学python的人都知道,python中一切皆是对象,如class生成的对象是对象,class本身也是对象,int是对象,str是对象,dict是对象....所以,我很好奇,python是怎样实现这些 ...

- VS2013编译python源码

系统:win10 手头有个python模块,是用C写的,想编译安装就需要让python调用C编译器.直接编译发现使用的是vc9编译,不支持C99标准(两个槽点:为啥VS2008都还不支持C99?手头这 ...

- 三种排序算法python源码——冒泡排序、插入排序、选择排序

最近在学习python,用python实现几个简单的排序算法,一方面巩固一下数据结构的知识,另一方面加深一下python的简单语法. 冒泡排序算法的思路是对任意两个相邻的数据进行比较,每次将最小和最大 ...

- 《python源码剖析》笔记一——python编译

1.python的架构: 2.python源码的组织结构: 3.windows环境下编译python:

- 转换器5:参考Python源码,实现Php代码转Ast并直接运行

前两个周末写了<手写PHP转Python编译器>的词法,语法分析部分,上个周末卡文了. 访问器部分写了两次都不满意,没办法,只好停下来,参考一下Python的实现.我实现的部分正好和Pyt ...

- python源码书籍

<Python源码剖析>一书现在很难买到,目前大部分都是电子书. 为了更好地利用Python语言,无论是使用Python语言本身,还是将Python与C/C++交互使用,深刻理解Pytho ...

- 类似py2exe软件真的能保护python源码吗

类似py2exe软件真的能保护python源码吗 背景 最近写了个工具用于对项目中C/C++文件的字符串常量进行自动化加密处理,用python写的,工具效果不错,所以打算在公司内部推广.为了防止代码泄 ...

- Python源码中的PyCodeObject

1.Python程序的执行过程 Python解释器(interpreter)在执行任何一个Python程序文件时,首先进行的动作都是先对文件中的Python源代码进行编译,编译的主要结果是产生的一组P ...

- Python源码学习(一)

考虑到性能的要求,我在工作中用的最多的是c/c++,然而,工作中又经常会有一些验证性的工作,这些工作对性能的要求并不高,反而对完成的效率要求更高,对于这样的工作,用一种开发效率高的语言是合理的想法,鉴 ...

随机推荐

- Python字典里的5个黑魔法

Python里面有3大数据结构:列表,字典和集合.字典是常用的数据结构,里面有一些重要的技巧用法,我把这些都整理到一起,熟练掌握这些技巧之后,对自己的功力大有帮助. 1.字典的排序: 用万金油sort ...

- Android重写HorizontalScrollView模仿ViewPager效果

Android提供的ViewPager类太复杂,有时候没有必要使用,所以重写一个HorizontalScrollView来实现类似的效果,也可以当做Gallery来用 思路很简单,就是重写onTouc ...

- Spark译文(二)

PySpark Usage Guide for Pandas with Apache Arrow(使用Apache Arrow的Pandas PySpark使用指南) Apache Arrow in ...

- C++入门经典-例5.10-指针作为返回值

1:代码如下: // 5.10.cpp : 定义控制台应用程序的入口点. // #include "stdafx.h" #include <iostream> usin ...

- opencv_将图像上的4个点按逆时针排序

1:代码如下: #include "stdafx.h" #include "cxcore.h" #include "cvcam.h" #in ...

- Hibernate持久化类规则

注意事项: 提供无参的构造方法,因为在hibernate需要使用反射生成类的实例 提供私有属性,并对这些属性提供公共的setting和getting方法,因为在hibernate底层会将查询到的数据进 ...

- CyclicBarrier源码阅读

一种允许多个线程全部等待彼此都到达某个屏障的同步机制 使用 多个线程并发执行同一个CyclicBarrier实例的await方法时,每个线程执行这个方法后,都会被暂停,只有当最后一个线程执行完awai ...

- spring boot 常用注解

@RestController和@RequestMapping注解 4.0重要的一个新的改进是@RestController注解,它继承自@Controller注解.4.0之前的版本,spring M ...

- 第11组 Beta冲刺(2/5)

第11组 Beta冲刺(2/5) 队名 不知道叫什么团队 组长博客 https://www.cnblogs.com/xxylac/p/11997386.html 作业博客 https://edu.cn ...

- java多线程系列3:悲观锁和乐观锁

1.悲观锁和乐观锁的基本概念 悲观锁: 总是认为当前想要获取的资源存在竞争(很悲观的想法),因此获取资源后会立刻加锁,于是其他线程想要获取该资源的时候就会一直阻塞直到能够获取到锁: 在传统的关系型数据 ...