Time Series_2_Multivariate_TBC!!!!

1. Cointegration

n×1 vector yt of time series is cointegrated if each series individually integrated in the order d (d = 1, nonstationary unit-root processes, i.e., random walks; d = 0, stationary process).

1.1 Simulation for Cointegration, based on Hamilton (1994)

#generate the two time series of length 1000

set.seed(20200229) #fix the random seed

N <- 100 #define length of simulation

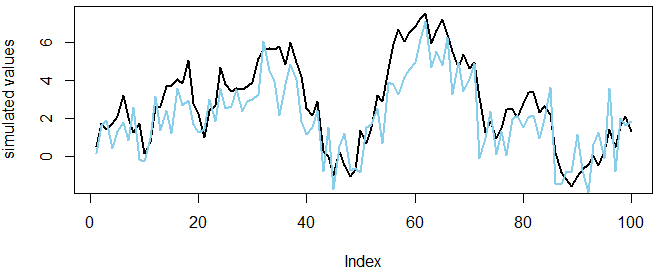

x <- cumsum(rnorm(N)) #simulate a normal random walk

gamma <- 0.7 #set an initial parameter value

y <- gamma * x + rnorm(N) #simulate the cointegrating series

plot(x, col="black", type='l', lwd=2, ylab='simulated values')

lines(y,col="skyblue", lwd=2)

Both series are individually random walks.

In real world we don't know gamma, so need estimation based on raw data, running linear regression of one series on the other, i.e., Engle-Granger method of testing cointegration.

1.2 Statistical Tests (Augmented Dickey Fuller test)

install.packages('urca')

library('urca')

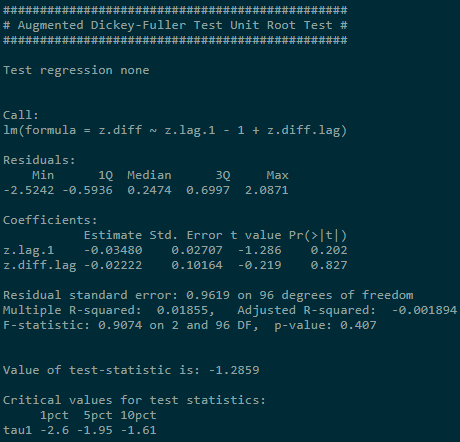

summary(ur.df(x,type="none"))

summary(ur.df(y,type="none"))

NULL: Unit root exists in the process

Reject NULL if test-statistic is smaller than critical value. Result shows test-statistic is larger than critical value at three usual sig.levels. We can't reject NULL.

Conclusion: Both series are individually unit root process.

1.3 Linear Combination

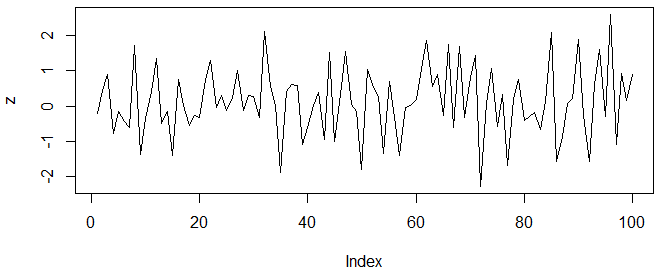

z <- y - gamma * x

plot(z,type='l')

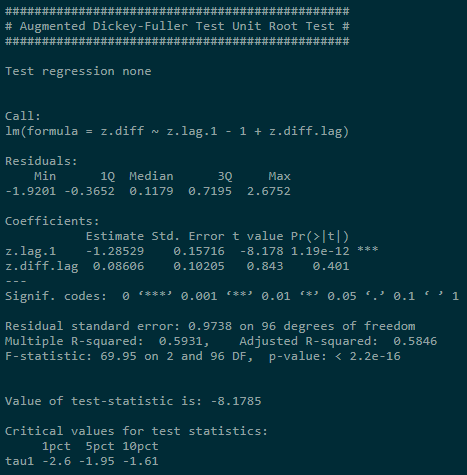

summary(ur.df(z,type="none"))

zt seems to be a white noise process and rejection of unit root if confirmed by ADF tests:

1.4 Estimate the Cointegrating Relationship using Engle-Granger method

Step 1: Run linear regression yt on xt (simple OLS estimation);

Step 2: Test residuals for the presence of a unit root.

coin <- lm(y ~ x -1) #regression without constant

coin$resid #obtain the residuals

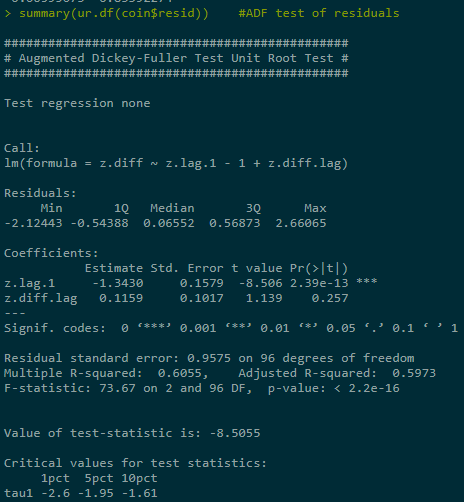

summary(ur.df(coin$resid)) #ADF test of residuals

Reject NULL.

Pair trading (statistical arbitrage) exploits such cointegrating relationship, aiming to set up strategy based on the spread between two time series. If two series are cointegrated, we expect their stationary linear combination to revert to 0. By selling relatively expensive and buying cheaper one, wait for the reversion to make profit.

Intuition: Linear combination of time series (which form cointegrating relationship) is determined by underlying (long-term) economic forces, e.g., same industry companies may grow similarly; spot and forward price of financial product are bound together by no-arbitrage principle; FX rates of interlinked countries tend to move together.

2. Vector Autoregressive Model

2.1 Theory Bgs

Ai are n×n coefficient matrices for all i = 1...p;

ut is a vector white noise process (assumes lack of auto correlation, while allow contemporaneous (同时发生的) correlation between components, i.e., ut has non-diagonal covariance matrix, meaning that contemporaneous dependencies aren't modeled) with positive definite covariance matrix. Thus we can use OLS to estimate equation by equation. (叫做 reduced form VAR models)

另一种叫做 structural VAR form model, SVAR models the contemporaneous effects among variables:

Where:

Disturbance terms are defined to be uncorrelated, thus are referred to as structural shocks.

2.2 Three-component VAR model (equity return, stock index, US Treasury bond interest rates)

2.2.1 Task: Forecast stock market index by using additional variables and identify impluse responses.

Assume: There exists a hidden long-term relationship between these three components.

2.2.2 Process:

rm(list = ls()) #clear the whole workspace

install.packages('xts');library(xts)

install.packages('vars');library('vars')

install.packages('quantmod');library('quantmod')

getSymbols('SNP', from='2012-01-02', to='2020-02-29')

getSymbols('MSFT', from='2012-01-02', to='2020-02-29')

getSymbols('DTB3', src='FRED') #3-month T-Bill interest rates

chartSeries(MSFT, theme=chartTheme('white'))

Cl(MSFT) #closing prices

Op(MSFT) #open prices

Hi(MSFT) #daily highest price

Lo(MSFT) #daily lowest price

ClCl(MSFT) #close-to-close daily return

Ad(MSFT) #daily adjusted closing price

Subset to obtain period of interests ,while the downloaded prices are supposed to be nonstationary series and should be transformed into stationary series:

#indexing time series data

DTB3.sub <- DTB3['2012-01-02/2020-02-29']

#Calculate returns from Adjusted log series

SNP.ret <- diff(log(Ad(SNP)))

MSFT.ret <- diff(log(Ad(MSFT)))

#replace NA values

DTB3.sub[is.na(DTB3.sub)] <- 0

DTB3.sub <- na.omit(DTB3.sub) # return with incomplete removed

# merge the three databases to get the same length

# innerjoin returns only rows in which one set have matching keys in the other

dataDaily <- na.omit(merge(SNP.ret,MSFT.ret,DTB3.sub), join='inner')

VAR modeling usually deals with lower frequency data, so transform data to monthly (or quarterly) frequency.

#obtain monthly data, package xts

SNP.M <- to.monthly(SNP.ret)$SNP.ret.Close

MSFT.M <- to.monthly(MSFT.ret)$MSFT.ret.Close

DTB3.M <- to.monthly(DTB3.sub)$DTB3.sub.Close

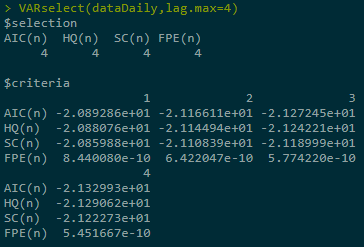

# allow a max of 4 lags

# choose the model with best(lowest Akaike Information Criterion value)

var1 <- VAR(dataDaily, lag.max=4, ic="AIC")

Or see multiple information criteria:

VARselect(dataDaily,lag.max=4)

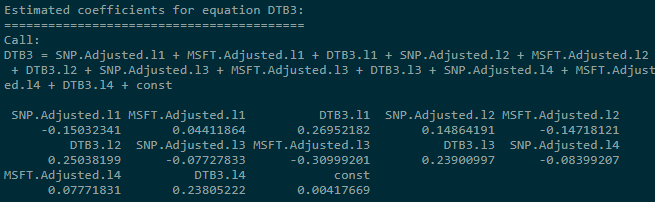

summary(var1)

coef(var1) #concise summary of the estimated variables

residuals(var1) #list of residuals (of the corresponding ~lm)

fitted(var1) #list of fitted values

Phi(var1) #coefficient matrices of VMA representation

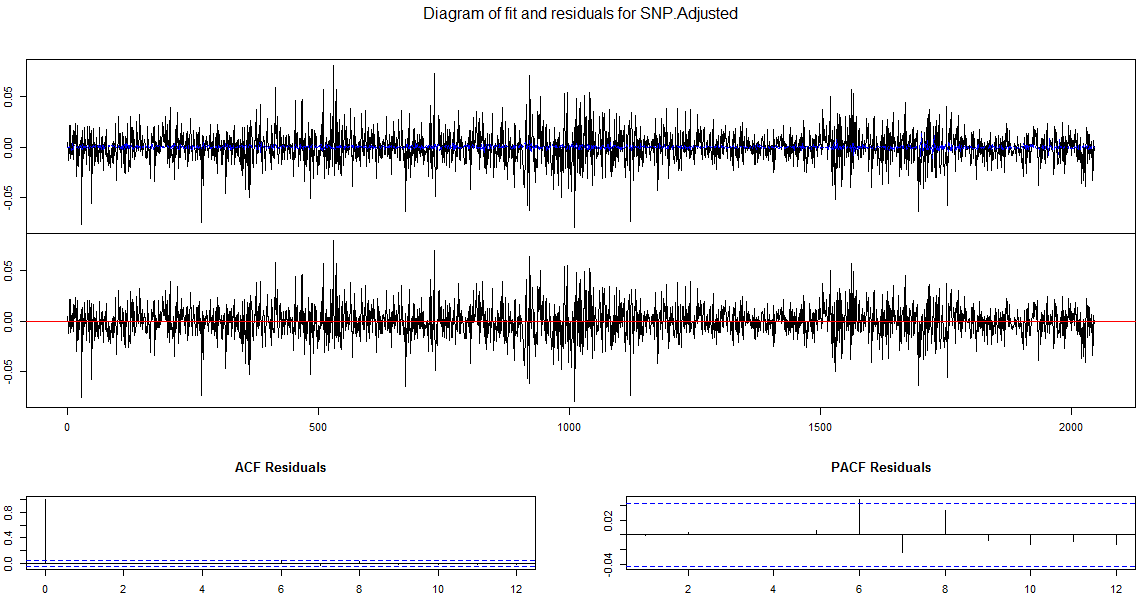

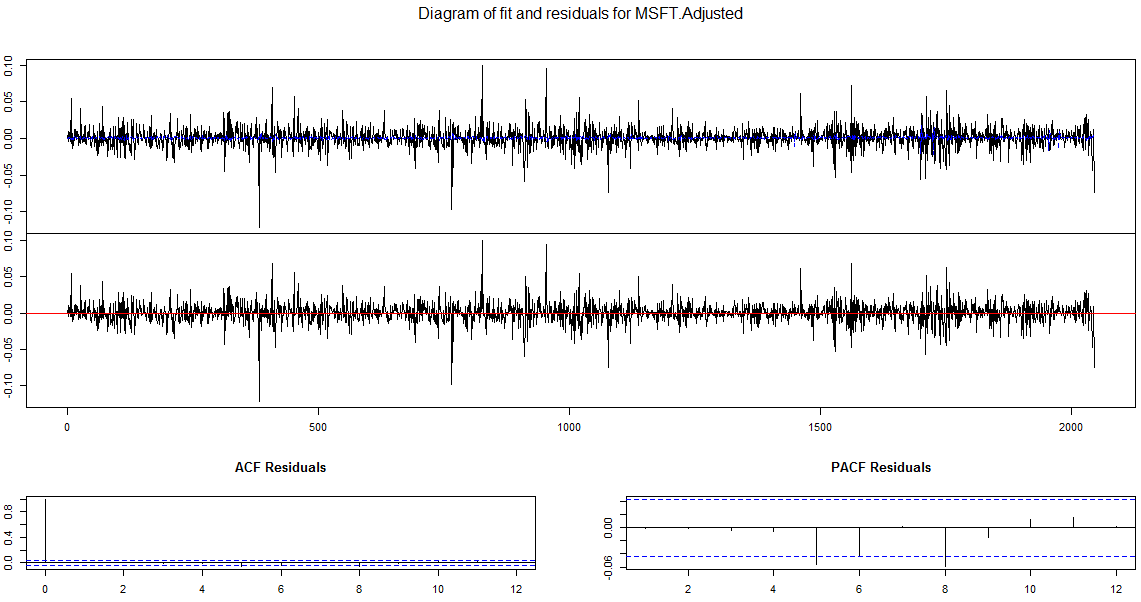

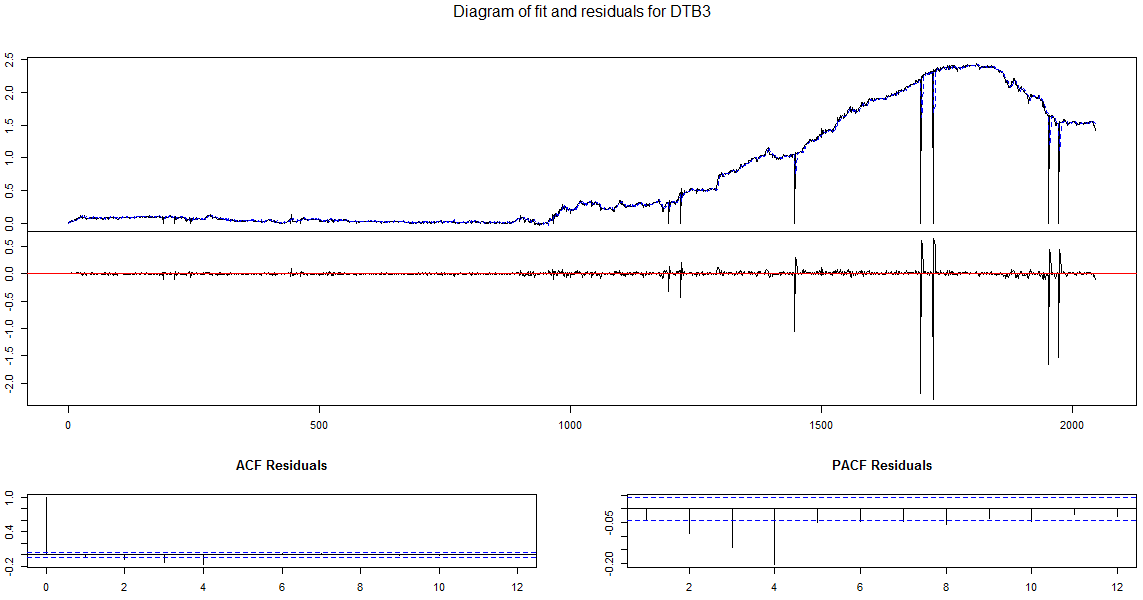

plot(var1, plot.type='multiple') #Diagram of fit and residuals for each variables

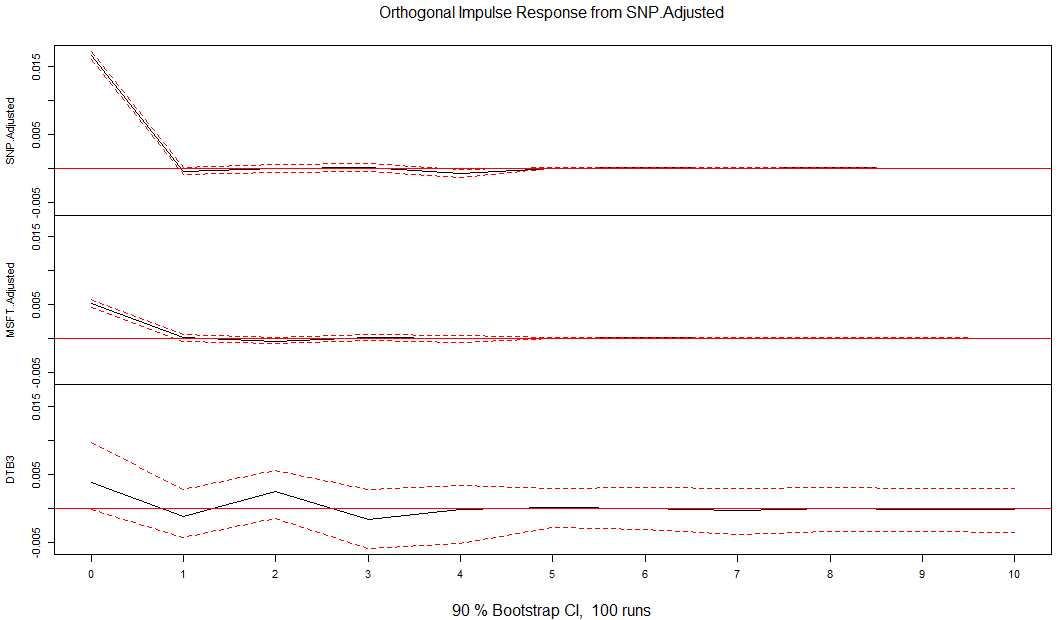

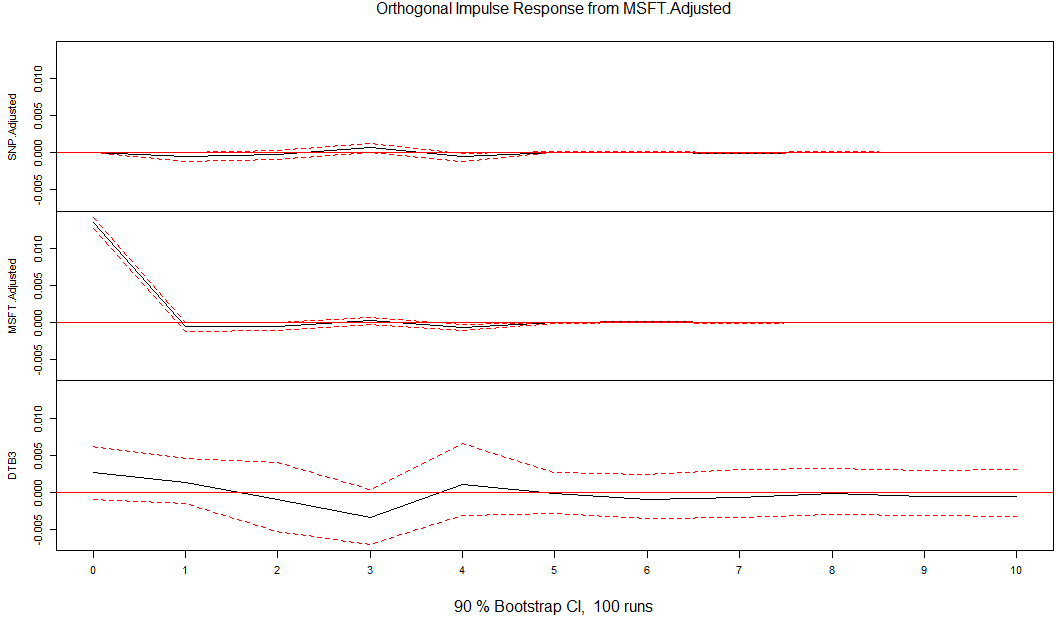

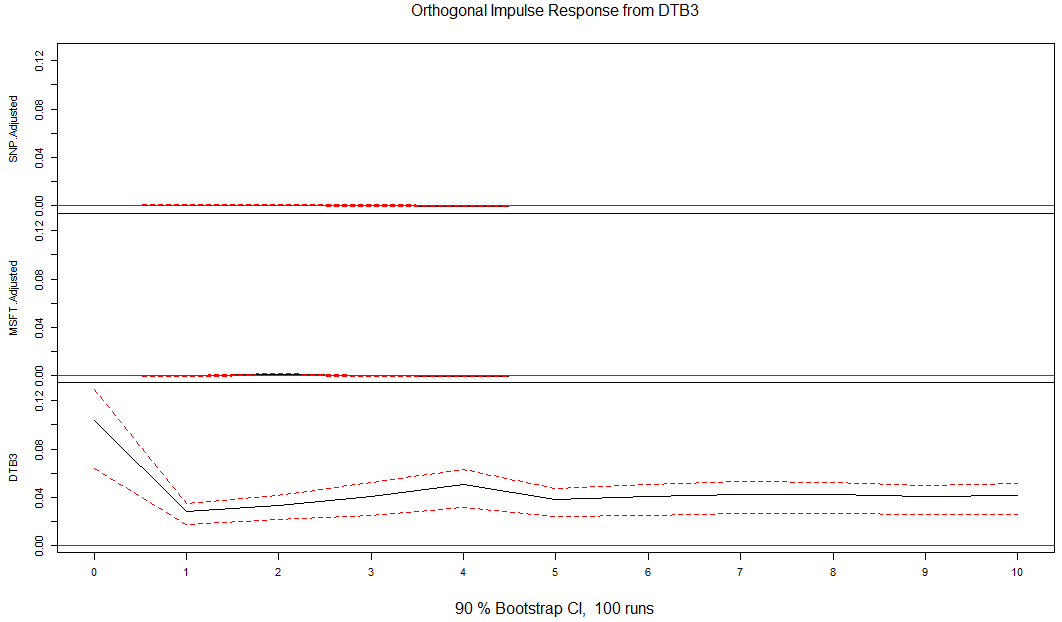

#confidence interval for bootstrapped error bands

var.irf <- irf(var1, ci=0.9)

plot(var.irf)

Number of required restrictions for SVAR model is K(K-1)/2, so in our case is 3.

Time Series_2_Multivariate_TBC!!!!的更多相关文章

随机推荐

- Deepin-linux下的linux的终端下软件安装和卸载方法

1.方法一: sudo apt update #最好第一步是它 sudo apt install <package_name> --no-upgrade #安装该package但是不升级. ...

- 【 hibernate 】基本配置

hibernate.cfg.xml <?xml version="1.0" encoding="UTF-8"?> <!DOCTYPE hibe ...

- 【PAT甲级】1044 Shopping in Mars (25 分)(前缀和,双指针)

题意: 输入一个正整数N和M(N<=1e5,M<=1e8),接下来输入N个正整数(<=1e3),按照升序输出"i-j",i~j的和等于M或者是最小的大于M的数段. ...

- 【译】索引进阶(十七): SQL SERVER索引最佳实践

[译注:此文为翻译,由于本人水平所限,疏漏在所难免,欢迎探讨指正] 原文链接:传送门. 在本章我们给出一些建议:贯穿本系列我们提取出了十四条基本指南,这些基本的指南将会帮助你为你的数据库创建最佳的索引 ...

- 如何为开发项目编写规范的README文件

前言 了解一个项目,首先都是通过其Readme文件了解信息.如果你以为Readme文件都是随便写写的那你就错了.github,oschina git gitcafe的代码托管平台上的项目的Readme ...

- 重新理解《务实创业》---HHR计划--以太一堂第三课

第一节:开始学习 1,面对创业和融资,我们应该如何从底层,理解他们的本质呢?(实事求是) 2,假设你现在要出来融资,通常你需要告诉投资人三件事:我的市场空间很大,我的用户需求很疼,我的商业模式能跑通. ...

- 图像分割利用KMeans生成灰度图

import numpy as np import PIL.Image as image from sklearn.cluster import KMeans def loadData(filePat ...

- spring demo

参考: https://www.tutorialspoint.com/spring/spring_applicationcontext_container.htm

- 基于Modelsim的视频流仿真

一.前言 最近在看牟新刚写的<基于FPGA的数字图像处理原理及应用>,书中关于FPGA数字图像处理的原理的原理写的非常透彻,在网上寻找了很久都没有找到完整的源代码工程,因此尝试自己做了补充 ...

- MessageBox函数

<Windows程序设计>(第五版)(美Charles Petzold著) https://docs.microsoft.com/zh-cn/windows/desktop/apiinde ...