Time Series_2_Multivariate_TBC!!!!

1. Cointegration

n×1 vector yt of time series is cointegrated if each series individually integrated in the order d (d = 1, nonstationary unit-root processes, i.e., random walks; d = 0, stationary process).

1.1 Simulation for Cointegration, based on Hamilton (1994)

#generate the two time series of length 1000

set.seed(20200229) #fix the random seed

N <- 100 #define length of simulation

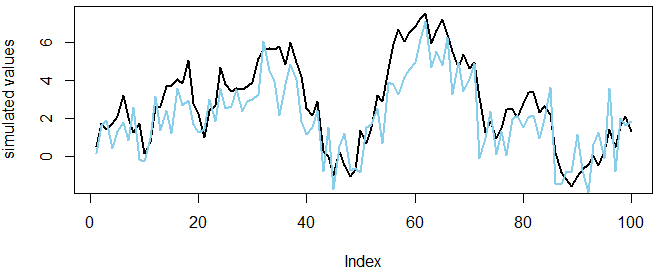

x <- cumsum(rnorm(N)) #simulate a normal random walk

gamma <- 0.7 #set an initial parameter value

y <- gamma * x + rnorm(N) #simulate the cointegrating series

plot(x, col="black", type='l', lwd=2, ylab='simulated values')

lines(y,col="skyblue", lwd=2)

Both series are individually random walks.

In real world we don't know gamma, so need estimation based on raw data, running linear regression of one series on the other, i.e., Engle-Granger method of testing cointegration.

1.2 Statistical Tests (Augmented Dickey Fuller test)

install.packages('urca')

library('urca')

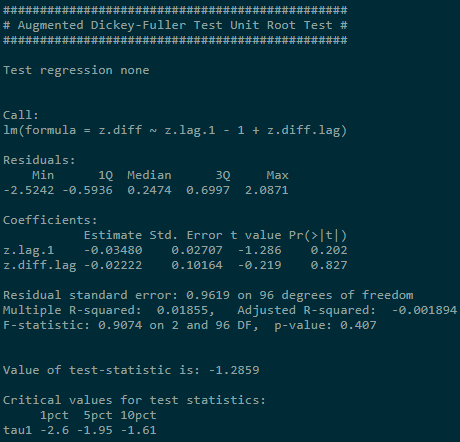

summary(ur.df(x,type="none"))

summary(ur.df(y,type="none"))

NULL: Unit root exists in the process

Reject NULL if test-statistic is smaller than critical value. Result shows test-statistic is larger than critical value at three usual sig.levels. We can't reject NULL.

Conclusion: Both series are individually unit root process.

1.3 Linear Combination

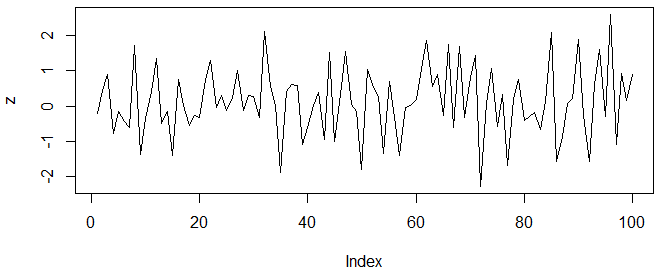

z <- y - gamma * x

plot(z,type='l')

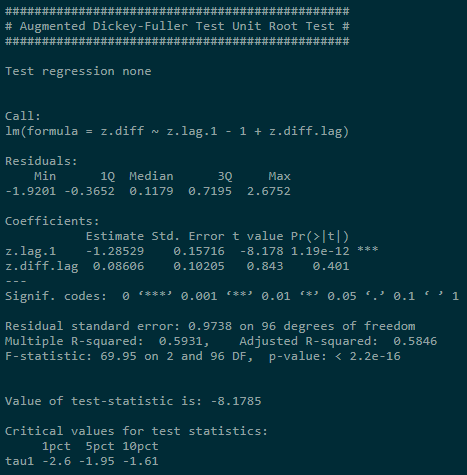

summary(ur.df(z,type="none"))

zt seems to be a white noise process and rejection of unit root if confirmed by ADF tests:

1.4 Estimate the Cointegrating Relationship using Engle-Granger method

Step 1: Run linear regression yt on xt (simple OLS estimation);

Step 2: Test residuals for the presence of a unit root.

coin <- lm(y ~ x -1) #regression without constant

coin$resid #obtain the residuals

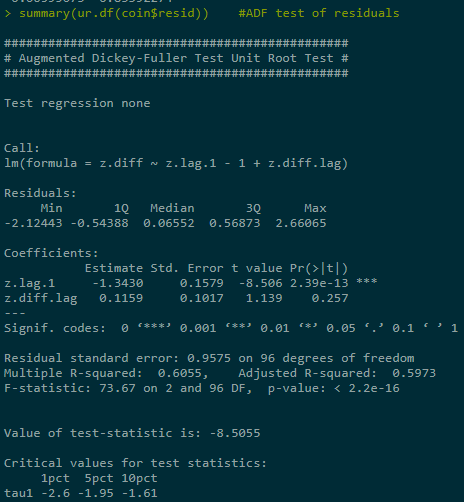

summary(ur.df(coin$resid)) #ADF test of residuals

Reject NULL.

Pair trading (statistical arbitrage) exploits such cointegrating relationship, aiming to set up strategy based on the spread between two time series. If two series are cointegrated, we expect their stationary linear combination to revert to 0. By selling relatively expensive and buying cheaper one, wait for the reversion to make profit.

Intuition: Linear combination of time series (which form cointegrating relationship) is determined by underlying (long-term) economic forces, e.g., same industry companies may grow similarly; spot and forward price of financial product are bound together by no-arbitrage principle; FX rates of interlinked countries tend to move together.

2. Vector Autoregressive Model

2.1 Theory Bgs

Ai are n×n coefficient matrices for all i = 1...p;

ut is a vector white noise process (assumes lack of auto correlation, while allow contemporaneous (同时发生的) correlation between components, i.e., ut has non-diagonal covariance matrix, meaning that contemporaneous dependencies aren't modeled) with positive definite covariance matrix. Thus we can use OLS to estimate equation by equation. (叫做 reduced form VAR models)

另一种叫做 structural VAR form model, SVAR models the contemporaneous effects among variables:

Where:

Disturbance terms are defined to be uncorrelated, thus are referred to as structural shocks.

2.2 Three-component VAR model (equity return, stock index, US Treasury bond interest rates)

2.2.1 Task: Forecast stock market index by using additional variables and identify impluse responses.

Assume: There exists a hidden long-term relationship between these three components.

2.2.2 Process:

rm(list = ls()) #clear the whole workspace

install.packages('xts');library(xts)

install.packages('vars');library('vars')

install.packages('quantmod');library('quantmod')

getSymbols('SNP', from='2012-01-02', to='2020-02-29')

getSymbols('MSFT', from='2012-01-02', to='2020-02-29')

getSymbols('DTB3', src='FRED') #3-month T-Bill interest rates

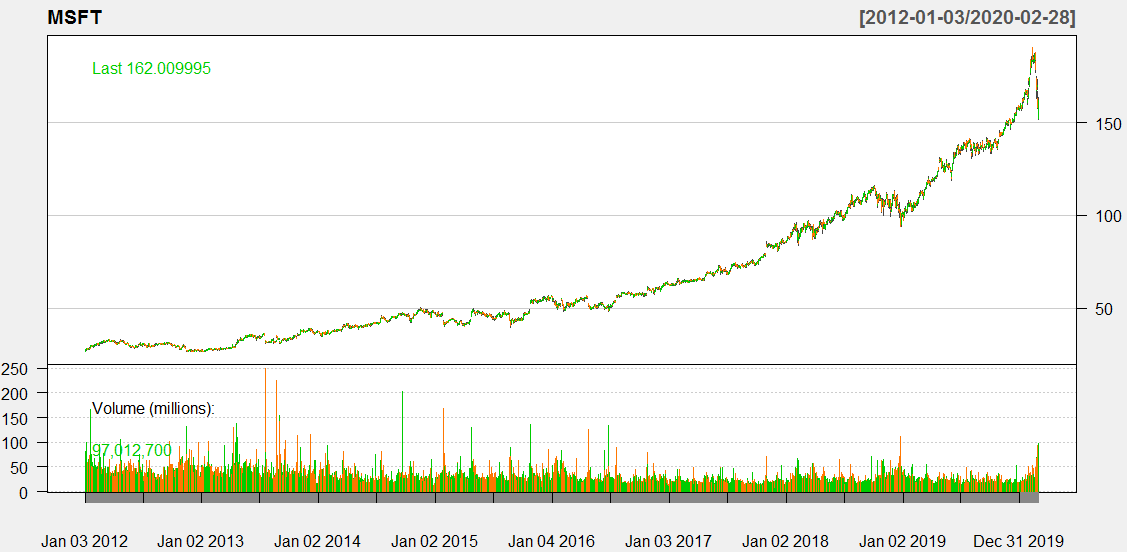

chartSeries(MSFT, theme=chartTheme('white'))

Cl(MSFT) #closing prices

Op(MSFT) #open prices

Hi(MSFT) #daily highest price

Lo(MSFT) #daily lowest price

ClCl(MSFT) #close-to-close daily return

Ad(MSFT) #daily adjusted closing price

Subset to obtain period of interests ,while the downloaded prices are supposed to be nonstationary series and should be transformed into stationary series:

#indexing time series data

DTB3.sub <- DTB3['2012-01-02/2020-02-29']

#Calculate returns from Adjusted log series

SNP.ret <- diff(log(Ad(SNP)))

MSFT.ret <- diff(log(Ad(MSFT)))

#replace NA values

DTB3.sub[is.na(DTB3.sub)] <- 0

DTB3.sub <- na.omit(DTB3.sub) # return with incomplete removed

# merge the three databases to get the same length

# innerjoin returns only rows in which one set have matching keys in the other

dataDaily <- na.omit(merge(SNP.ret,MSFT.ret,DTB3.sub), join='inner')

VAR modeling usually deals with lower frequency data, so transform data to monthly (or quarterly) frequency.

#obtain monthly data, package xts

SNP.M <- to.monthly(SNP.ret)$SNP.ret.Close

MSFT.M <- to.monthly(MSFT.ret)$MSFT.ret.Close

DTB3.M <- to.monthly(DTB3.sub)$DTB3.sub.Close

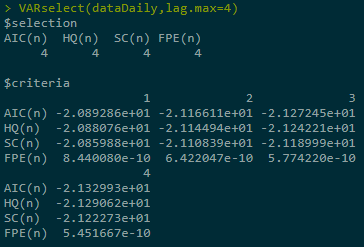

# allow a max of 4 lags

# choose the model with best(lowest Akaike Information Criterion value)

var1 <- VAR(dataDaily, lag.max=4, ic="AIC")

Or see multiple information criteria:

VARselect(dataDaily,lag.max=4)

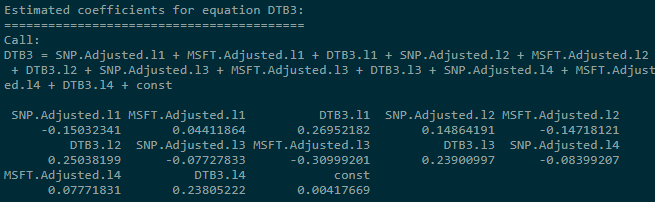

summary(var1)

coef(var1) #concise summary of the estimated variables

residuals(var1) #list of residuals (of the corresponding ~lm)

fitted(var1) #list of fitted values

Phi(var1) #coefficient matrices of VMA representation

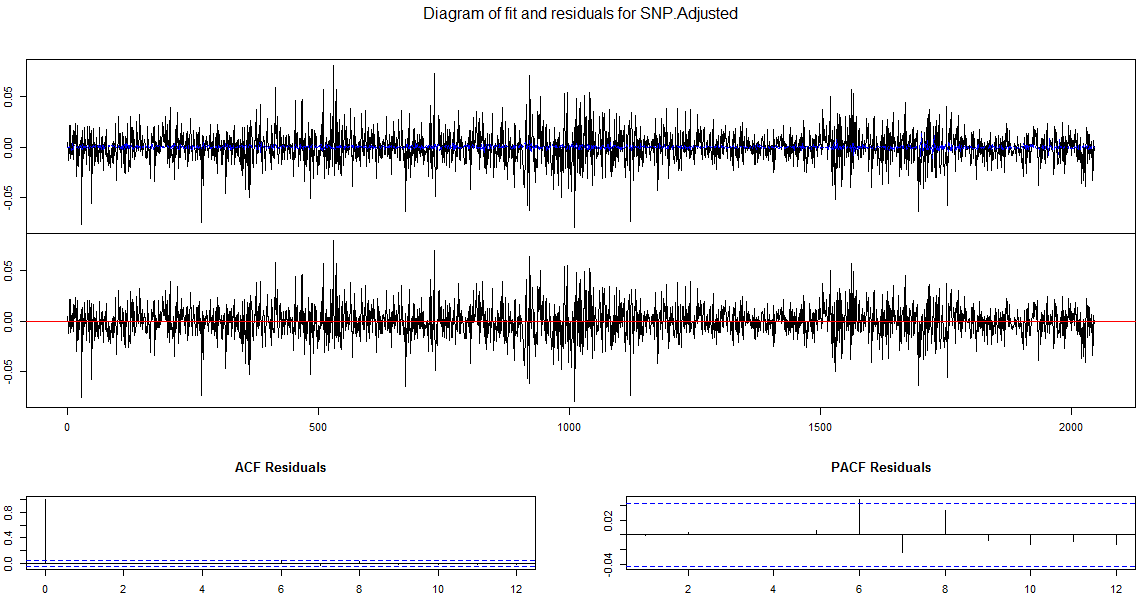

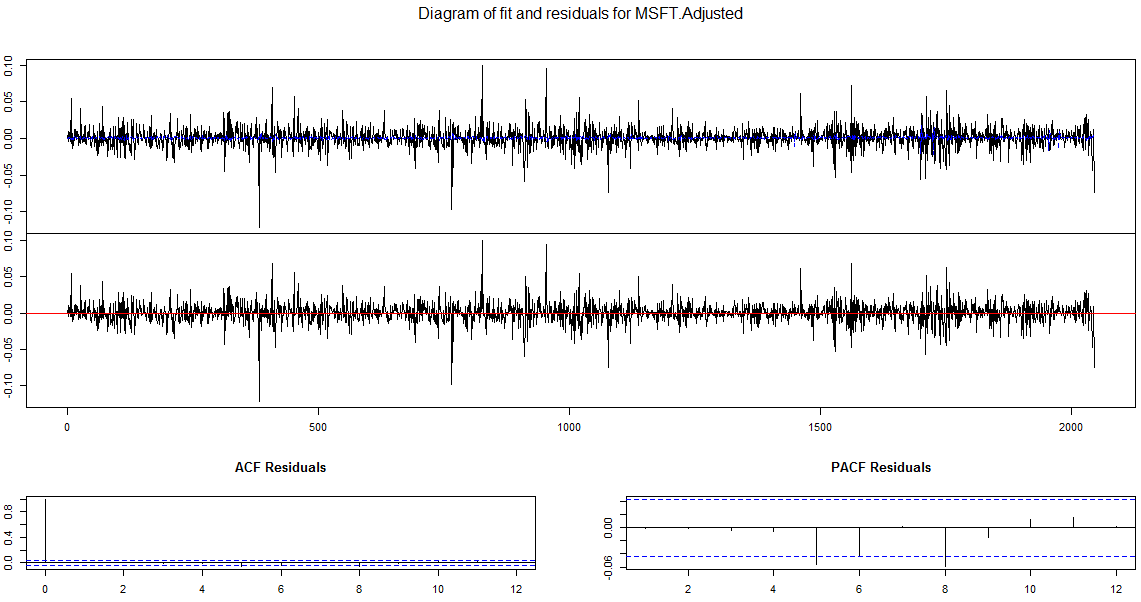

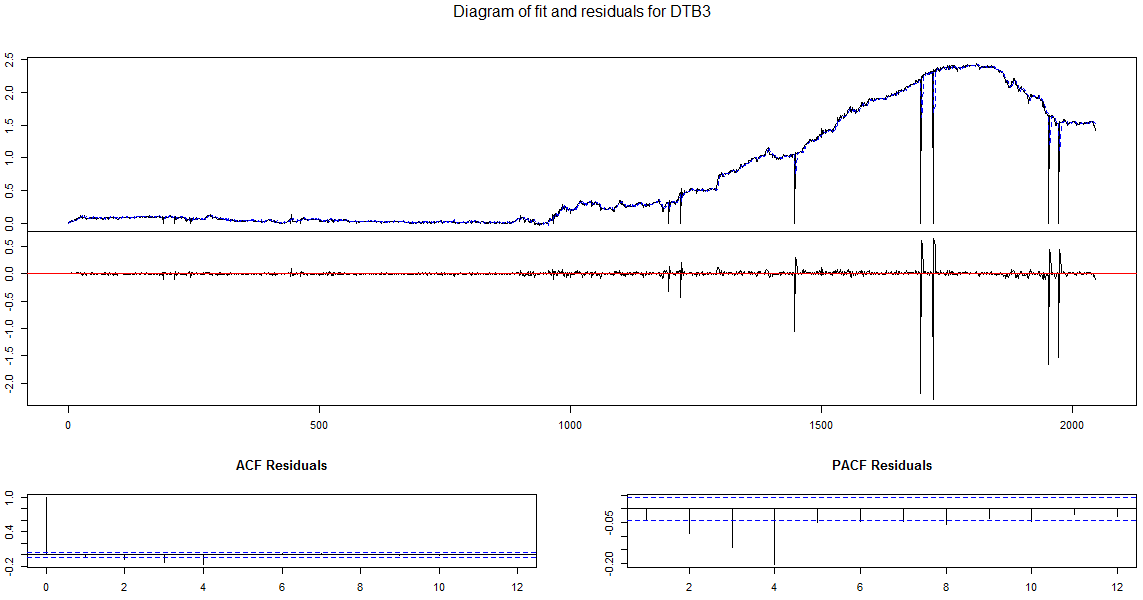

plot(var1, plot.type='multiple') #Diagram of fit and residuals for each variables

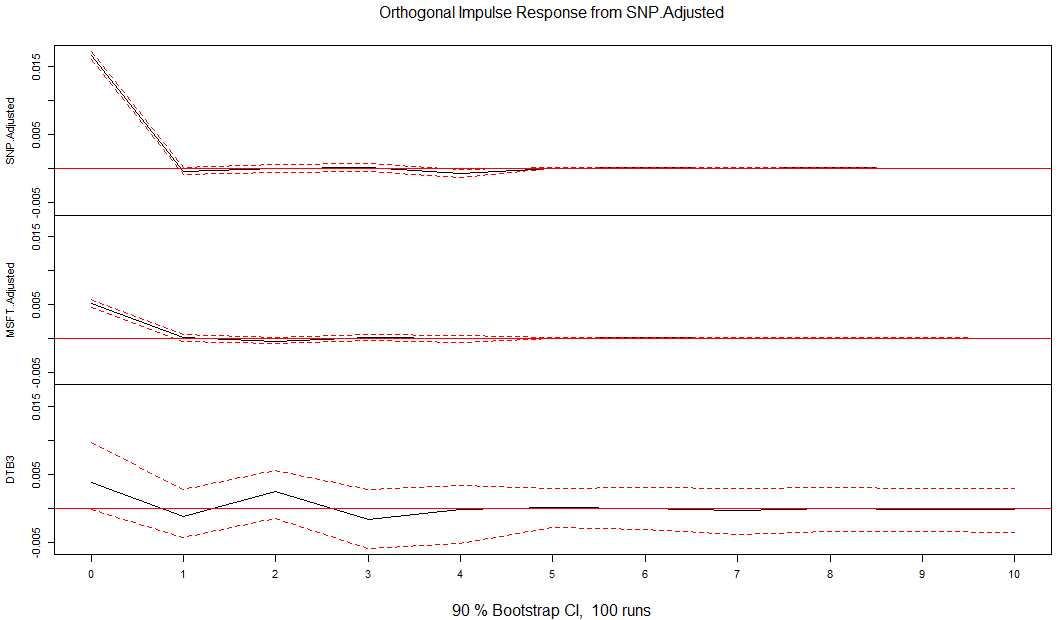

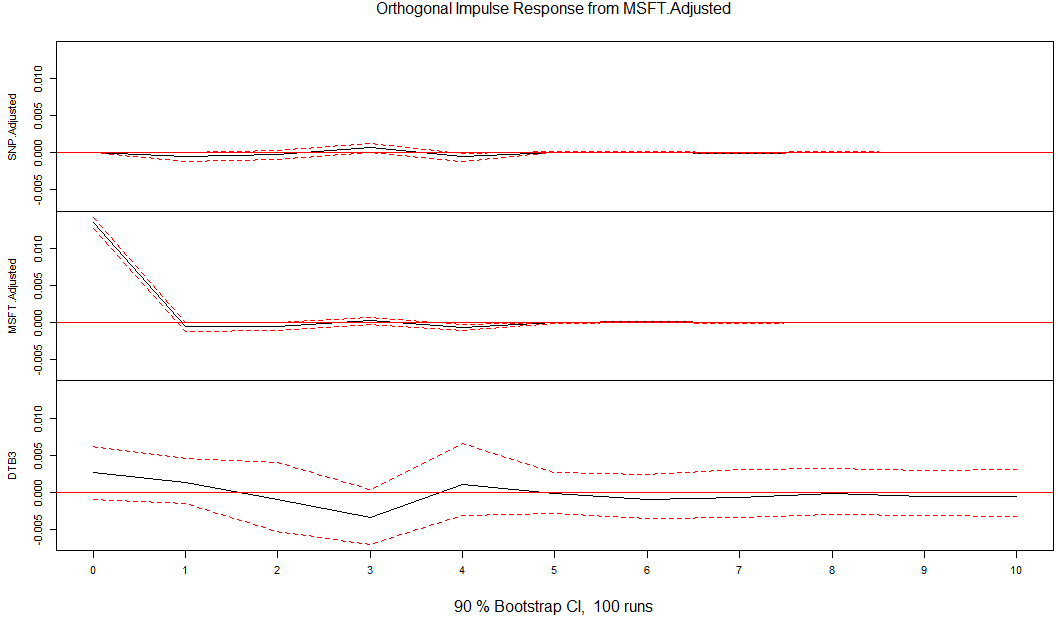

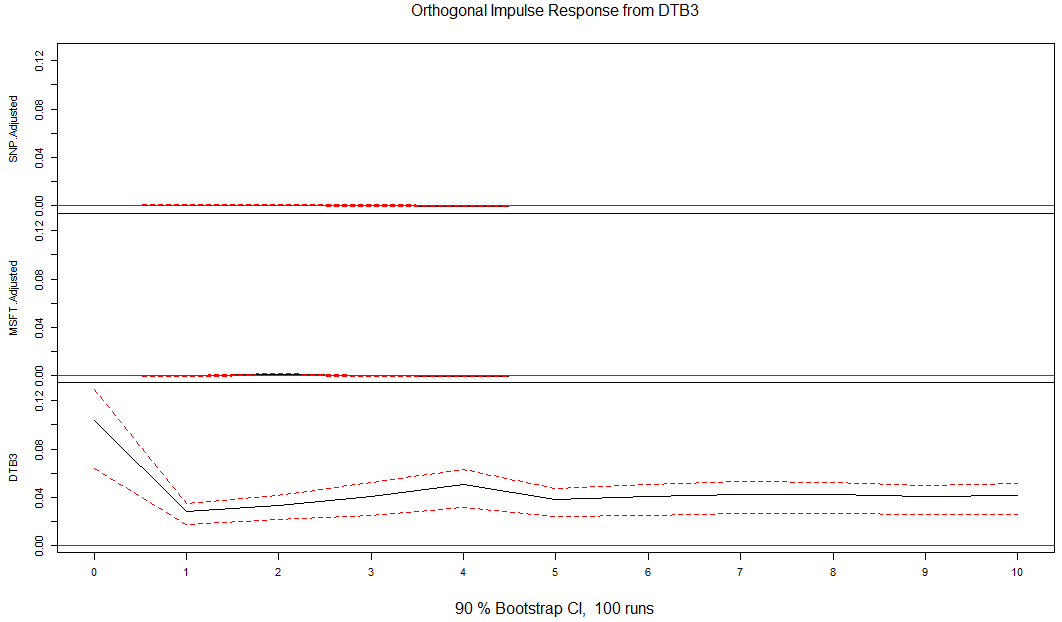

#confidence interval for bootstrapped error bands

var.irf <- irf(var1, ci=0.9)

plot(var.irf)

Number of required restrictions for SVAR model is K(K-1)/2, so in our case is 3.

Time Series_2_Multivariate_TBC!!!!的更多相关文章

随机推荐

- 基于scikitlearn的深度学习环境安装(三)(完整版)

OS Linux Ubuntu14.04 安装 pip (python2.7.9或以上自带pip) sudo apt-get install python-pip pip是python环境下安装包的 ...

- 23 JavaScript规范与最佳实践&性能&箭头函数

大多数web服务器(Apache等)对大小写敏感,因此命名注意大小写 不要声明字符串.数字和布尔值,始终把他们看做原始值而非对象,如果把这些声明为对象,会拖慢执行速度 对象是无法比较的,原始值可以 不 ...

- SSL 证书格式普及,PEM、CER、JKS、PKCS12

根据不同的服务器以及服务器的版本,我们需要用到不同的证书格式,就市面上主流的服务器来说,大概有以下格式: .DER .CER,文件是二进制格式,只保存证书,不保存私钥. .PEM,一般是文本格式,可保 ...

- java里自定义分页查询的尝试

public String list(){ try { LoginUser loginUser = getLoginUser();//获取当前登录用户 if(curpage<=0){ curpa ...

- 科幻电影免费百度云分享(Scince-fiction cloud share)

Marvel episode Link Passcode:6h9k Star War full episode Link Passcode:7abk Men In Black Episode Col ...

- SD-WAN功能

SD-WAN功能 在这些底层技术的基础之上,SD-WAN最终能为客户提供哪些创新型服务.解决哪些具体问题? 统一管理与监控:SD-WAN整合了路由器.防火墙.DPI检测.广域网加速等功能,确保企业真正 ...

- python3.6.5修改print的颜色

开头部分:\033[显示方式;前景色;背景色m +想要输出的内容:\033[0m 注意:开头部分的三个参数:显示方式,前景色,背景色是可选参数,具体参数效果见下文,可以只写其中的某一个:参数 ...

- JavaScript - Array对象,数组

1. 创建数组 方式1. new关键字 var arr = new Array(1, 2, 3); 方式2. 使用字面量创建数组对象 var arr = [1, 2, 3]; 2. 检测一个对象是否是 ...

- nginx防盗链处理模块referer和secure_link模块

使用场景:某网站听过URI引用你的页面:当用户在网站点击url时:http头部会通过referer头部,将该网站当前页面的url带上,告诉服务本次请求是由这个页面发起的 思路:通过referer模块, ...

- Microsoft Cortana移动版除美国市场外不再可用

导读 先前已经透露,Microsoft Cortana的移动版本已不复存在.目前,Microsoft Cortana在移动设备上的多个国家和地区中支持多种语言.微软的Cortana移动版本不再支持的市 ...