【原】Coursera—Andrew Ng机器学习—编程作业 Programming Exercise 1 线性回归

作业说明

Exercise 1,Week 2,使用Octave实现线性回归模型。数据集 ex1data1.txt ,ex1data2.txt

单变量线性回归必须实现,实现代价函数计算Computing Cost 和 梯度下降Gradient Descent。

多变量线性回归可选,实现 特征Feature Normalization、代价函数计算Computing Cost 、 梯度下降Gradient Descent 和 Normal Equations 。

文件清单

- ex1.m

- ex1_multi.m

- ex1data1.txt - ex1.m 用到的数据组

- ex1data2.txt - ex1_multi.m 用到的数据组

- submit.m - 提交代码

- [*] warmUpExercise.m

- [*] plotData.m

- [*] computeCost.m

- [*] gradientDescent.m

- [+] computeCostMulti.m

- [+] gradientDescentMulti.m

- [+] featureNormalize.m

- [+] normalEqn.m

* 为必须要完成的

+ 为可

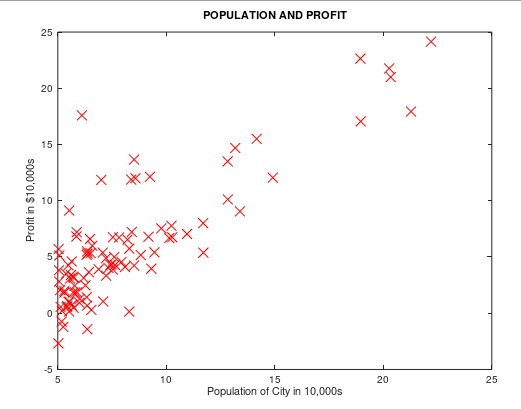

背景:假设我们现在是个连锁餐厅的老板,已经在很多城市开了连锁店(提供训练组),现在想再开新店,需要通过以前的数据预测新开的店的收益。

ex1data1.txt 提供所需要的训练组,第一列是城市人口,第二列是对应的收益。负值代表着亏损。

结论

当数据的特征维度比较小的时候,使用正规方程方法不需要进行特征归一化,而且结果稳定。梯度下降有可能得到局部最优解,导致结果不同。

注意矩阵计算的一些问题,求和前面一项需要转置。

必做题 单变量线性回归

一、warmUp

单变量线性回归入口在ex1.m

warmUpExercise.m

A = eye()

二、绘制数据图

我实现的 plotData.m:

plot(x,y,'rx', 'MarkerSize', );

xlabel('Population of City in 10,000s');

ylabel('Profit in $10,000s');

title('POPULATION AND PROFIT');

ex1.m 中的调用:

%% ======================= Part : Plotting ======================= data = load('ex1data1.txt');

X = data(:, ); y = data(:, );

m = length(y); % number of training examples

plotData(X, y);

运行效果如下:

三、代价函数

我实现的 computeCost.m:

function J = computeCost(X, y, theta) m = length(y); % number of training examples

J = ;

predictions = X * theta; % predictions of hapothesis on all m examples

sqrErrors = (predictions - y) .^ ; % squared errors .^ 指的是对数据中每个元素平方 J = / ( * m) * sum(sqrErrors);

end

四、梯度下降

我实现的 gradientDescent.m

矩阵性质:(AB)T =BTAT

function [theta, J_history, theta_history] = gradientDescent(X, y, theta, alpha, num_iters) m = length(y); % number of training examples

J_history = zeros(num_iters, );

theta_history = zeros(, num_iters); % 【改动】使用 ×iteration维矩阵,保存theta每次迭代的历史 for iter = :num_iters % 这里为了方便理解 拆的比较细,可以组合成一步操作 theta = theta - (alpha / m) * X' * (X * theta - y)

% prediction h(x) m×2矩阵 * 2×1向量 = m维列向量

predictions = X * theta;

% error h(x)-y m维列向量

errors = predictions - y; %

% derivative of J() m维行向量 * m×2矩阵 = 2维列向量

lineLope = X' * errors;

% theta 2维列向量

theta = theta - (alpha / m) * lineLope; %

J_history(iter) = computeCost(X, y, theta); % Save the cost J in every iteration

theta_history(:,iter) = theta; % 给theta_history 第iter列赋值

end end

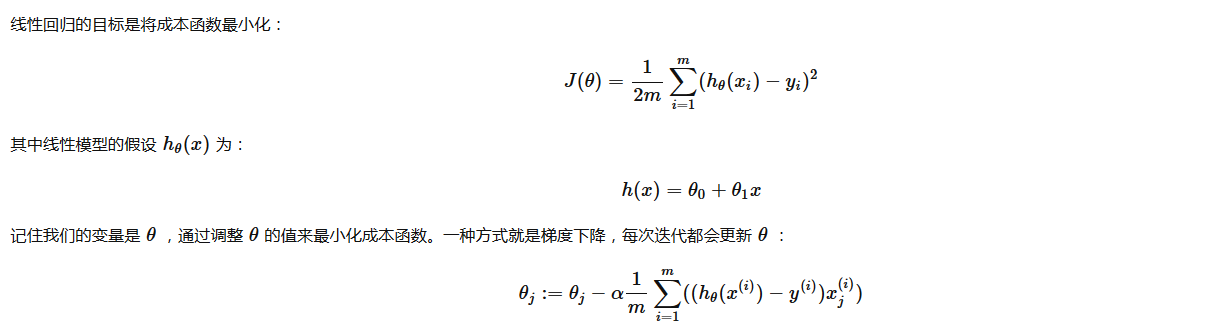

五、绘制预测曲线

ex1.m 中的调用:

%% =================== Part : Cost and Gradient descent =================== % 设置 X 和 theta

X = [ones(m, ), data(:,)]; % Add a column of ones to x

theta = zeros(, ); % initialize fitting parameters % 设置迭代次数和学习速率

iterations = ;

alpha = 0.01;

% compute and display initial cost 计算theta=[;]时代价

J = computeCost(X, y, theta);

% further testing of the cost function 计算theta=[-;]时代价

J = computeCost(X, y, [- ; ]);

fprintf('\nRunning Gradient Descent ...\n') % 【改动1】改为获取多个返回值,J_history保存每次迭代的代价,theta保存每次迭代的theta0和theta1

% 原:theta = gradientDescent(X, y, theta, alpha, iterations);

[theta,J_history,theta_history] = gradientDescent(X, y, theta, alpha, iterations); % Plot the linear fit 在数据图上绘制最终的拟合直线

hold on; % keep previous plot visible

plot(X(:,), X*theta, '-')

legend('Training data', 'Linear regression')

hold off % don't overlay any more plots on this figure

运行结果如下:

四、绘制cost和theta变化曲线

自己加的功能。在ex1.m中增加以下代码,绘制图像。展示迭代过程中 cost 和 theta 的变化曲线

% --------------【改动2】绘制代价和theta变化曲线 start --------------

fprintf('Size of J_history saved by gradient descent:\n');

fprintf('%f\n', size(J_history));

iterX = [:iterations]'; % 生成图像横坐标,迭代次数 % 绘左侧图,展示迭代过程中代价的变化曲线

subplot(,,);

plot(iterX, J_history, '-','linewidth',); % 绘制代价函数曲线

title('cost of each step'),

xlabel('iteration'),ylabel('value of cost'),

legend('value of cost'); % 绘右侧图,展示迭代过程中theta的变化曲线

theta0_history = theta_history(,:);

theta1_history = theta_history(,:);

subplot(,,);

plot(iterX,theta0_history,'-','linewidth',);

hold on;

plot(iterX,theta1_history,'-','linewidth',,'color','r');

title('theta of each step'),xlabel('iteration'),ylabel('value of theta'),legend('theta0','theta1');

% --------------【改动2】绘制代价和theta变化曲线 end -------------- % Predict values for population sizes of , and ,

predict1 = [, 3.5] * theta;

fprintf('For population = 35,000, we predict a profit of %f\n',...

predict1*);

predict2 = [, ] * theta;

fprintf('For population = 70,000, we predict a profit of %f\n',...

predict2*);

输出如下:

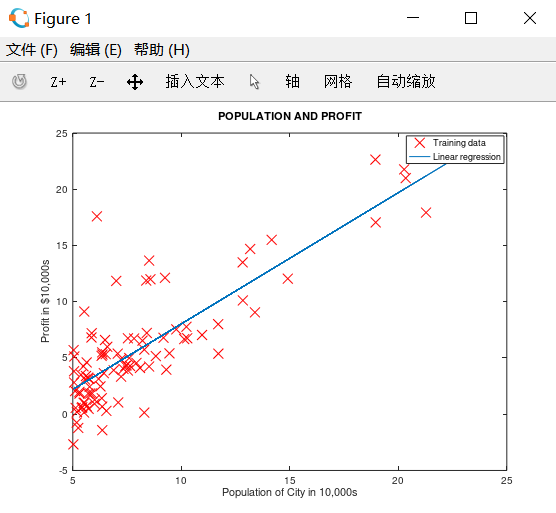

五、绘制代价函数三维曲线 和 等高线图

ex1.m 调用:

1、初始化 theta0 为(-10,10)均分100个点,theta1 为(-1,4)均分100个点,J_vals 为100 * 100的数组

这里使用了Matlab中的均分计算指令 linspace(x1,x2,N) ,用于产生x1、x2之间的N点行线性的矢量。其中x1、x2、N分别为起始值、终止值、元素个数。默认N为100。

2、循环计算每组(theta0,theta1),用 J_vals 保存对应的代价cost。

%% ============= Part : Visualizing J(theta_0, theta_1) =============

fprintf('Visualizing J(theta_0, theta_1) ...\n') % Grid over which we will calculate J

theta0_vals = linspace(-, , );

theta1_vals = linspace(-, , ); % initialize J_vals to a matrix of 's

J_vals = zeros(length(theta0_vals), length(theta1_vals)); % Fill out J_vals

for i = :length(theta0_vals)

for j = :length(theta1_vals)

t = [theta0_vals(i); theta1_vals(j)];

J_vals(i,j) = computeCost(X, y, t);

end

end % Because of the way meshgrids work in the surf command, we need to

% transpose J_vals before calling surf, or else the axes will be flipped

J_vals = J_vals';

% Surface plot

figure;

surf(theta0_vals, theta1_vals, J_vals)

xlabel('\theta_0'); ylabel('\theta_1'); % Contour plot

figure;

% Plot J_vals as contours spaced logarithmically between 0.01 and

contour(theta0_vals, theta1_vals, J_vals, logspace(-, , ))

xlabel('\theta_0'); ylabel('\theta_1');

hold on;

plot(theta(), theta(), 'rx', 'MarkerSize', , 'LineWidth', );

3、将theta0作为X坐标,theta1作为Y坐标,J_vals作为Z坐标,绘制三维图形

4、将theta0作为X坐标,theta1作为Y坐标,绘制J_vals的等高线图

5、在等高线图中,标记上面求出的使代价函数最小的 theta0,theta1点的位置。在等高线中心

这些图像的目的是为了展示 随着Θ0 和 Θ1 的改变,J值的变化。(在2D轮廓图中比3D的更直观)。最小点是Θ0 和 Θ1最适点, 每一步梯度下降都会更靠近这个点。

可以通过旋转看到为什么叫“轮廓图”:

选做 多变量线性回归

一 、特征归一化

需要用特性放缩让数据的范围缩小,使得梯度下降计算的更快:

- 计算每个特性的平均值(mean)

- 计算标准差(standard deviations)

- 特性放缩(feature scaling)

* 这里利用的是标准差(standard deviation),也可以使用差值(max - min)。

featureNormalize.m 如下:

1 function [X_norm, mu, sigma] = featureNormalize(X)

7

9 X_norm = X;

10 mu = zeros(1, size(X, 2)); % 1行,列数和X相同

11 sigma = zeros(1, size(X, 2));

12

13 % ====================== YOUR CODE HERE ======================

29 mu = mean(X);

30 sigma = std(X);

32 X_norm = (X_norm - mu) ./ sigma;

35

36 end

二、代价函数和梯度下降

因为在单变量线性回归中,使用的是向量化的计算方法,对于多变量线性回归同样适用。不需要重新写

computeCostMulti.m 和 computCost.m 一样,gradientDescentMulti.m 和gradientDescent.m 一样

ex1_multi.m 里的调用:

%% ================ Part : Gradient Descent ================

alpha = 1.2;

num_iters = ; % Init Theta and Run Gradient Descent

theta = zeros(, );

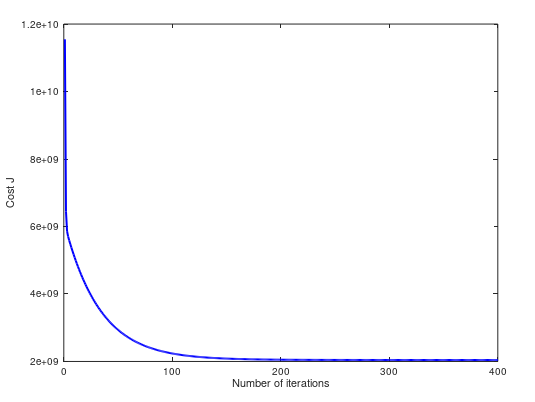

[theta,J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters); % Plot the convergence graph

figure;

plot(:numel(J_history), J_history, '-b', 'LineWidth', );

xlabel('Number of iterations');

ylabel('Cost J'); % Estimate the price of a sq-ft, br house

% 这里要注意,需要把输入的值进行 normalize,然后才能代入预测方程中

predict_x = [,];

predict_x = (predict_x - mu) ./ sigma;

price = [, predict_x] * theta;

三、正规方程

公式:

normalEqn.m 实现:

function [theta] = normalEqn(X, y)

theta = zeros(size(X, ), );

theta = pinv(X' * X) * X' * y

end

ex1_multi 里的调用:

%% ================ Part : Normal Equations ================

% predict the price of a sq-ft, br house. data = csvread('ex1data2.txt'); % 重新加载数据

X = data(:, :);

y = data(:, );

m = length(y);

% Add intercept term to X

X = [ones(m, ) X];

% Calculate the parameters from the normal equation

theta = normalEqn(X, y); % 使用正规方程进行计算

28 % ====================== YOUR CODE HERE ======================

price = [, , ] * theta; % 预测结果 % ============================================================

四、测试

运行结果:

Loading data ...

First examples from the dataset:

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

x = [ ], y =

Program paused. Press enter to continue.

Normalizing Features ...

1.00000000 0.13000987 -0.22367519

1.00000000 -0.50418984 -0.22367519

1.00000000 0.50247636 -0.22367519

1.00000000 -0.73572306 -1.53776691

1.00000000 1.25747602 1.09041654

1.00000000 -0.01973173 1.09041654

1.00000000 -0.58723980 -0.22367519

1.00000000 -0.72188140 -0.22367519

1.00000000 -0.78102304 -0.22367519

1.00000000 -0.63757311 -0.22367519

1.00000000 -0.07635670 1.09041654

1.00000000 -0.00085674 -0.22367519

1.00000000 -0.13927334 -0.22367519

1.00000000 3.11729182 2.40450826

1.00000000 -0.92195631 -0.22367519

1.00000000 0.37664309 1.09041654

Running gradient descent ...

Theta computed from gradient descent:

334302.063993

100087.116006

3673.548451

(1)当 α = 0.05,预测一个1650 sq-ft, 3 br house 的房屋的售价。梯度下降和正规方程的预测值不同:

68 Predicted price of a 1650 sq-ft, 3 br house (using gradient descent):

69 $289314.620338

81

82 Predicted price of a 1650 sq-ft, 3 br house (using normal equations):

83 $293081.464335

(2)当 α = 0.15,cost 曲线如下。两个方法预测值都是 $293081.464335:

(3)当 α = 1,cost 曲线如下。两个方法预测值都是 $293081.464335:

(4)当 α = 1.2,cost 曲线如下。两个方法预测值都是 $293081.464335:

(5)当 α = 1.3,cost 曲线如下。两个方法预测值不同 $293157.248289 ,$293081.464335:

完整代码:https://github.com/madoubao/coursera_machine_learning/tree/master/homework/machine-learning-ex1/ex1

【原】Coursera—Andrew Ng机器学习—编程作业 Programming Exercise 1 线性回归的更多相关文章

- 【原】Coursera—Andrew Ng机器学习—编程作业 Programming Exercise 4—反向传播神经网络

课程笔记 Coursera—Andrew Ng机器学习—课程笔记 Lecture 9_Neural Networks learning 作业说明 Exercise 4,Week 5,实现反向传播 ba ...

- 【原】Coursera—Andrew Ng机器学习—编程作业 Programming Exercise 2——逻辑回归

作业说明 Exercise 2,Week 3,使用Octave实现逻辑回归模型.数据集 ex2data1.txt ,ex2data2.txt 实现 Sigmoid .代价函数计算Computing ...

- 【原】Coursera—Andrew Ng机器学习—编程作业 Programming Exercise 3—多分类逻辑回归和神经网络

作业说明 Exercise 3,Week 4,使用Octave实现图片中手写数字 0-9 的识别,采用两种方式(1)多分类逻辑回归(2)多分类神经网络.对比结果. (1)多分类逻辑回归:实现 lrCo ...

- Andrew Ng机器学习编程作业: Linear Regression

编程作业有两个文件 1.machine-learning-live-scripts(此为脚本文件方便作业) 2.machine-learning-ex1(此为作业文件) 将这两个文件解压拖入matla ...

- Andrew Ng机器学习编程作业:Logistic Regression

编程作业文件: machine-learning-ex2 1. Logistic Regression (逻辑回归) 有之前学生的数据,建立逻辑回归模型预测,根据两次考试结果预测一个学生是否有资格被大 ...

- Andrew Ng机器学习编程作业:Regularized Linear Regression and Bias/Variance

作业文件: machine-learning-ex5 1. 正则化线性回归 在本次练习的前半部分,我们将会正则化的线性回归模型来利用水库中水位的变化预测流出大坝的水量,后半部分我们对调试的学习算法进行 ...

- Andrew NG 机器学习编程作业5 Octave

问题描述:根据水库中蓄水标线(water level) 使用正则化的线性回归模型预 水流量(water flowing out of dam),然后 debug 学习算法 以及 讨论偏差和方差对 该线 ...

- Andrew NG 机器学习编程作业4 Octave

问题描述:利用BP神经网络对识别阿拉伯数字(0-9) 训练数据集(training set)如下:一共有5000个训练实例(training instance),每个训练实例是一个400维特征的列向量 ...

- Andrew NG 机器学习编程作业3 Octave

问题描述:使用逻辑回归(logistic regression)和神经网络(neural networks)识别手写的阿拉伯数字(0-9) 一.逻辑回归实现: 数据加载到octave中,如下图所示: ...

随机推荐

- java事务(三)——自己实现分布式事务

在上一篇<java事务(二)——本地事务>中已经提到了事务的类型,并对本地事务做了说明.而分布式事务是跨越多个数据源来对数据来进行访问和更新,在JAVA中是使用JTA(Java Trans ...

- eclipse新建web项目

方法/步骤 首先,你要先打开Eclipse软件,打开后在工具栏依次点击[File]>>>[New]>>>[Dynamic Web Project],这个就代 ...

- HTML的后缀显示、标准格式和标签(1)

后缀的显示 win10:打开我的计算机--->点击上面的查看--->选中文件扩展名 win8:打开我的计算机--->点击上面的组织选中文件夹选项--->点击上面的查看---&g ...

- FindBugs初探

1. 什么是FindBugs FindBugs 是一个静态分析工具,它检查类或者 JAR 文件,将字节码与一组缺陷模式进行对比以发现可能的问题.有了静态分析工具,就可以在不实际运行程序的情况对软件进行 ...

- flash游戏服务器安全策略

在网页游戏开发中,绝大多数即时通信游戏采用flash+socket 模式来作为消息数据传递.在开发过程中大多数开发者在开发过程中本地没有问题,但是一旦部署到了网络,就存在连接上socket服务器.究 ...

- 配置文件Struts.xml 中type属性 redirect,redirectAction,chain的区别

1.redirect:action处理完后重定向到一个视图资源(如:jsp页面),请求参数全部丢失,action处理结果也全部丢失. 2.redirectAction:action处理完后重定向到一 ...

- 利用Github免费搭建个人主页(个人博客)

之前闲着, 利用Github搭了个免费的个人主页. 涉及: Github注册 Github搭建博客 域名选购 绑定域名 更多 一 Github注册 在地址栏输入地址:http://github.co ...

- verilog中function的使用

函数的功能和任务的功能类似,但二者还存在很大的不同.在 Verilog HDL 语法中也存在函数的定义和调用. 1.函数的定义 函数通过关键词 function 和 endfunction 定义,不允 ...

- Anaconda 使用conda常用命令

1.首先在所在系统中安装Anaconda.可以打开命令行输入conda -V检验是否安装以及当前conda的版本. 2.conda常用的命令. 1)conda list 查看安装了哪些包. 2)con ...

- Redis官方文档》持久化

原文链接 译者:Alexandar Mahone 这篇文章从技术层面描述了Redis持久化,建议所有读者阅读.如果希望更多了解Redis持久化和持久性保障,建议阅读Redis持久化揭秘. Redis ...